Opinion | The Neymar Vortex

Opinion | The Neymar Vortex

How valuation and optionality are inversely correlated

Vanity and pride are different things, though the words are often used synonymously. A person may be proud without being vain. Pride relates more to our opinion of ourselves, vanity to what we would have others think of us.”

- Jane Austen, Pride and Prejudice

Edit: On September 10, 2019, Stripe announced a competitor, Stripe Corporate Card. The path ahead looks a lot more difficult now.

Pity Neymar.

Last night, Europe’s transfer window closed, leaving one of football’s* most gifted players stranded on a team that wants to sell him, unable to join a team that wants to buy him. The problem, of course, is one of valuation.

It could all have been so different. In the summer of 2017, Neymar had the world at his feet. Not only was he the ostensible heir-apparent to Ronaldo and Messi, he had recently become the world’s most expensive player, joining Paris Saint-Germain (PSG) for a record $263MM, rising to as much as $500MM over the course of his five-year deal. He was hailed as the future of an insurgent franchise, ready to take the next step and become a European elite.

Yet there was a feeling at the time, that for all its glitz, Neymar had taken a step down. He’d traded winning titles for individual awards, he’d swapped a lavish salary for an absurd one, he’d sacrificed being a part of something greater than himself with being a solitary star; he mortgaged optionality for vanity. In doing so, he brought in to being the Neymar Vortex, an unlucky spot in which genuine success is over-recognized and results in counter-productive pricing.

To be clear: this is the fault of investors, whether they be football clubs or venture capitalists.

In the latter camp, with more money available than ever, investors are increasingly bidding against each other, and in trying to move more quickly that their peers, are willing to jump a multiple (or more) to get a deal over the line. Irrational and ill-disciplined, this behavior is presenting more and more founders with a conundrum: take the best offer the market gives me (and hope to grow into it), or undervalue myself?

As self-serving as it sounds, I think that in instances in which there is an exceptional delta between the best and median offer, or between the current offer and last round, the latter is preferable — because it preserves optionality. Raising at too high a valuation requires a business to either ‘catch up’, or become efficient enough to no longer need outside capital. In cases in which that is not possible, the remaining options are unattractive for all involved: down rounds, distressed sales, financial engineering, closure.

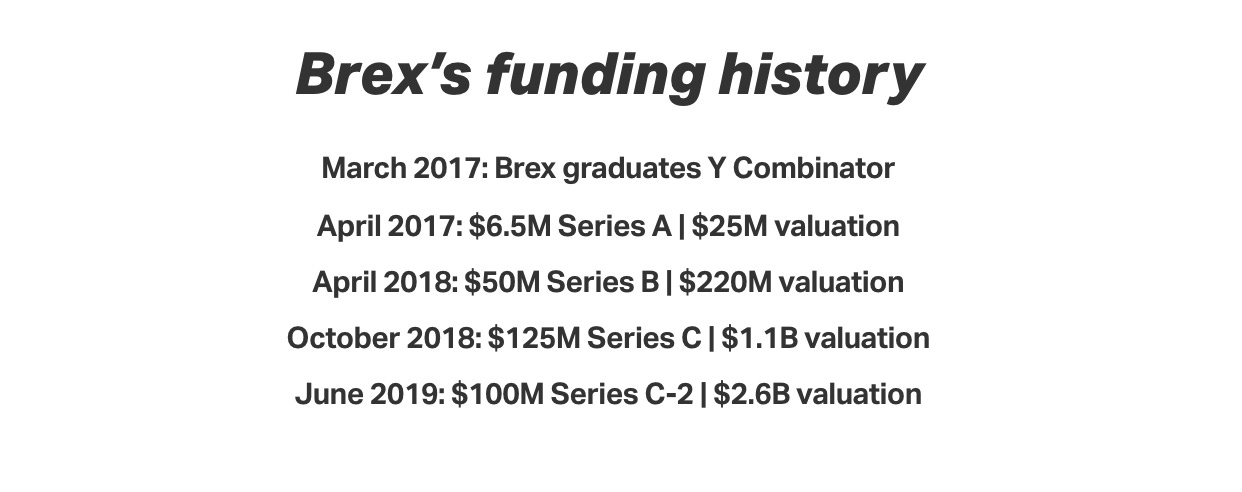

Earlier this summer, banking startup Brex raised an $100MM Series C-2, valuing the company at $2.6B. A little over half a year before, the company raised $125MM at a $1.1B valuation. In an interview with Techcrunch, Brex’s CEO Henrique Dubugras noted that an increased total addressable market (TAM) size was behind the change. This is intriguing in that it is not directly tied to the company’s growth — in other words, it seems to reflect a somewhat ineffable increase in investor confidence rather than something tied to a particular set of metrics.** Moreover, Dubugras noted that company was yet to touch the $125MM raised in October; rather, this was simply a “repricing event.” Two months later, New York competitor Ramp announced its fundraise.

I do not know what will happen to Neymar, or Brex, or the other companies that I believe have raised at inflated valuations. (I await the cull of the scooter co’s). In Neymar’s case, he will likely be forced to sit on the sidelines before a return to Spain in January. In Brex’s case, they may become the dominant financial provider for the next-generation of companies making $2.6B look very cheap, indeed.

High valuations can do a great deal of good. They come with press, eager candidates, money, itself. But in an irrational market in which startups stay private longer and rely on venture financing to a greater extent, optionality is the stronger currency.

—

{kind=link}

** It could very well be that Brex does not want to disclose the metrics question.