Palantir and the Chaos Dance

From the S-1 Club

Palantir in 1 minute

Palantir is the most political IPO of 2020, as well as an enigmatic business. Part software firm, part consultancy, the brainchild of Peter Thiel is at the center of a culture war. Is it ethical to service the Immigration and Customs Enforcement agency in Trump's America? Is it treasonous not to? Palantir's primary challenges may not be matters of product or market, but politics and public perception.

The firm lists 17 years after its inception with a revenue run rate of $962M, recent growth of 49%, and gross margins of 55% at scale. Palantir is not profitable and lost $580M in 2019. Winners of the IPO include Thiel and the venture capital firm he created, Founders Fund.

To learn about Palantir's CIA funding, role in bringing down organized crime, and unique business model, read on.

If you enjoy this analysis, sign up for more S-1s here 👇

Analysts

Introduction

Palantir is an ethical dilemma disguised as a company. Is it the punitive enabler of an administration's xenophobia or the stout defender of liberal democracy? Is it a services business — Uncle Sam's dev shop — or a software company? Like the blot of ink in a Rorschach test, the answer depends at least as much on you as it does the boundaries of light and dark.

The company's S-1 is in no such doubt. It is, in its brazenness, a remarkable document. Explicitly political whenever possible, and written — in parts — with the flair and dramatic tension of a thriller, the bombast of a stump speech.

Alex Karp, Palantir's CEO, ends an opening letter with a line that would not be out of place in an Aaron Sorkin vehicle, all staccato delivery and swelling instrumentals:

"We have chosen sides, and we know that our partners value our commitment. We stand by them when it is convenient, and when it is not."

Later, the filing outlines the company's efforts in transforming the work of those on the front-lines of global conflict. The passage ends with a sentence, poetic in its restraint.

"The stakes are high."

For a corporate document, this is unusual writing and high-drama. We mean this as a compliment — Palantir is master of their message with a clarity few companies achieve. For much of the opening salvo, Karp and Co. seem to be channeling the iconic "you can't handle the truth” scene in A Few Good Men. We, the observing public, want Palantir on that wall, need them on that wall, whether we admit it or not. They protect us beneath a blanket of freedom; it is not ours to question how it is provided.

A figure lurks in the spaces between and beneath words. Peter Thiel: the ghost in the machine, making a palimpsest of what is printed.

If there's any unifying philosophy to the iconoclastic founder of PayPal, Palantir, and investment vehicles including Founders Fund, the ill-fated Clarium Capital, and Mithril Capital (he really likes Lord of the Rings), it's a belief in the merits of volatility. In periods of instability, opportunities to drive rapid progress are made more possible.

In part, Palantir shares that interest. Though reliant on the support of formal, established power — governments, primarily — the company trades off chaos. A disordered world, awhirl with asymmetric threats, needs Palantir more acutely than a stable one. In deriving its strength from disarray, there is something antifragile about the firm. (We know we have summoned a swarm of fastidious Talebites with the invocation.)

Such is the curious weltanschauung of Thiel. In order and disorder, structure and tumult, he dances. An artist of decay, but also an eliminator of it. If Rome is burning, Thiel is not the fiddler but the enterprising profiteer selling bags of sand out the back of his chariot, returning a week later with kindling.

In its forthrightness and subtlety, self-assurance and defensiveness, Palantir's S-1 is an embodiment of its creator.

Number of mentions in the S-1

Government: 230

Alexander Karp or Karp: 60

Peter Thiel or Thiel: 44

Military: 13

Allies: 13

Chinese communist party: 3

Palantir’s history

After selling PayPal for $1.5B, Peter Thiel had money and time. In 2003, the year after eBay's acquisition of the payments company, he set out to tackle arguably the most consequential challenge faced by the United States: thwarting terror attacks.

This was, after all, not far removed from 9/11. Already, Thiel had realized the value of data in solving complex problems. At PayPal, the firm had instituted a fraud-detection algorithm called "IGOR," a solution that garnered the FBI's interest. Thiel felt that model could be applied to other problems, namely identifying and tracking potential threats to national security.

Though he had the money to fund it, Thiel didn't have the coding chops to get it off the ground. To bring his vision to life, he set about recruiting some old friends: Joe Lonsdale and Stephen Cohen from his Stanford days, and Nathan Gettings from PayPal. The foursome came together to build a data-mining engine, named — as would become something of a Thiel convention — after an artifact from the Lord of the Rings universe.

The "palantíri" or "seeing stones" allow observers to see across realms, scanning both past and future. After all, that was what America needed, wasn't it?

Finding a leader

Though Thiel backed the company in its early days, Palantir nevertheless sought additional capital.

It was a struggle to begin with — Thiel decided hiring a more seasoned CEO might help. He interviewed a slew of such candidates; passed on them all. Perhaps he consulted a seeing stone because he emerged with an unlikely candidate — a wizard with a grab bag of academic degrees, no technology or government background, and little additional experience. Thiel tapped former Stanford Law classmate, verbal sparring pal, and avowed bachelor-for-life Alex Karp, PhD.

Karp in 2012, Business Insider

It turned out to be an inspired choice.

Gaining traction

With Karp onboard, the team secured funding from In-Q-Tel, the Central Intelligence Agency's (CIA) venture arm in 2005. They then spent the next few years (2005-2008) working with the CIA data to train Palantir's analytics engine. That early boost was invaluable. With a working product and influential connections, it wasn't long before Palantir began to reel in government, military, and police department contracts.

During those years, few civilians knew about Palantir. The company landed on the radar of more Americans after it was reported to have helped track down Osama Bin Laden in 2011. It started to win recognition in the defense community and notoriety among skeptics and conspiracy theorists. Despite that publicity, some in the tech community questioned whether or not Palantir's software was effective at all, noting that most of its engagements with clients seemed to be service engagements rather than SaaS.

As the company grew, it did little to counteract its reputation as secretive, almost cultic. The secrecy makes sense given the nature of Palantir's work; many employees have security clearances and can't discuss their work publicly. Perhaps the cultic feel derives from the fact employees call themselves "Palantirians" and the home office "the Shire." Or, as one employee put it:

Palantir sees itself as a collective of unlikely heros [sic] — think X-Men with glasses — who are out to defeat evildoers wherever they may lurk.

Public backlash

Given the company's client base, perhaps it was inevitable Palantir might face a backlash. Tossing aside any questions around how "pure-play" Palantir's software is, some of Palantir's products seem to have worked almost too well, evoking the dystopian worlds of Person of Interest, Minority Report, and Brazil.

Predictably, the public has taken notice. The company has been attacked for ethics and privacy violations associated with a number of their government and policing projects. One of the most significant controversies to date has been Palantir's alleged involvement in the Immigration and Customs Enforcement (ICE) agency's deportation efforts. It was reported by WNYC that, in 2019, Palantir's software helped identify illegal immigrants, allowing government forces to raid their workplaces and deport families. Palantir's software was similarly alleged to have been used by ICE to plan a raid in 2018 on 98 Seven-Eleven stores with undocumented workers. Palantir has also helped the police departments of Los Angeles and New Orleans "profile" citizens, using data to "forecast criminal behavior."

Will this matter to public market investors? Other government contractors, including Raytheon, General Dynamics, and Northrop Grumman, have their own chequered paths. All have overcome public outcries of one form or another.

Preparing to go public

Palantir is a late bloomer. The company that started around the time that Facebook launched (the early 2000s) and five years after Google did, and is only now heading to the public markets.

Indeed, for a time, it seemed as if Palantir would never go public, by choice. Management knew that full exposure of its work might lead to censure. Palantir received substantial pushback from some employees and investors over this, contributing to the decision to file.

In preparation, Palantir made efforts to expand its investor appeal, including bringing a woman onto the Board of Directors. Alexandra Wolfe Schiff was previously a reporter at the Wall Street Journal. Beyond that, the company has also expanded from its initial target market (government agencies, police, and military), embracing the private sector. Today, the company has 125 customers and serves non-profit and private sector customers across industries, from banking to automotive to airlines.

Even though Palantir is going public, it's twisting the definition of what that means. Management has created a multi-class shareholder model, ensuring they remain in the driver's seat indefinitely. (See "Management team" for more). That may be for ideological reasons as much as for financial ones — the company is transparent in its ambition to elevate "the West," eschewing China's possible riches. From Karp:

"We will make the West, especially America, the strongest in the world, the strongest it's ever been, for the sake of global peace and prosperity."

Market

As stated in the introductory section of its S-1, Palantir sells "[a] generalizable platform for modeling the world and making decisions." How should we evaluate the market for that?

To do so, we must first understand the reach of the company's product. The company has built two principal software platforms — Palantir Gotham ("Gotham") and Palantir Foundry ("Foundry"). Gotham came first, built shortly after Palantir's founding in 2003, and was created specifically for the United States intelligence community to assist in counterterrorism investigations and operations. Gotham's use has now extended beyond intelligence and counterterrorism, into defense operations and mission planning. Next, Palantir realized that many institutions — not just the US government — face the same "needle in a haystack" data challenges. They built their Foundry product to solve that problem for commercial enterprises. At the time of the S-1, Palantir products were being used by 125 customers across 150 countries and 36 industries, including intelligence, defense, energy, transportation, financial series, and healthcare.

Part of the Gotham platform, Palantir’s S-1 filing

Part of the Foundry platform, Palantir’s S-1 filing

As we evaluate the market into which Palantir is selling its product, the right question to ask moves pretty quickly from who is a customer to who isn't a customer:

As noted earlier, the Palantir management team appears to have decided to only sell their product to the "United States, its allies, and countries abroad whose values align with liberal democracies." Regardless of whether you classify this as a philosophical or business decision, it's a helpful data point as we evaluate the size of Palantir's public sector opportunity.

Gotham and Foundry are expensive, long term investments built to solve complex problems. Therefore they are likely not a fit for small and medium-sized businesses — this is decidedly an enterprise product. Palantir estimates that there are approximately 6,000 companies globally, with more than $500M in annual revenue that could be potential customers.

Taken together, Palantir believes that the total addressable market for its business is $119B: $26B in US public sector opportunity, $37B in international public sector opportunity, and $56B in private sector commercial opportunity. The public sector TAM estimates are based on financial statistics published by the International Monetary Fund on spending across government sectors and the assumption that 5% of that expenditure was for software and consulting services. An overview of Palantir’s sectoral expansion here:

Palantir’s S-1 filing

This TAM breakdown of public vs. private and US vs. international is interesting because it foreshadows what Palantir believes to be a few of its vital growth opportunities:

Given the commercial opportunity is greater than the government opportunity, Palantir will continue to expand into the sector. In 2019, 53% of revenue came from commercial customers, and 47% came from government agencies.

Given the international government opportunity is greater than selling solely to the United States, Palantir will continue to expand reach with US allies abroad. As mentioned, 40% of 2019 revenue was from customers in the US, and the remaining 60% was from customers abroad.

Getting back to first principles — is this a good market to sell software products into? The answer is both yes and no. Palantir has a long uphill battle towards customer acquisition but benefits from stickiness and contract expansion. Unlike other enterprise software businesses, Palantir can essentially expand contracts in perpetuity because of its focus on governments.

Product

While we mentioned the two primary products above, the full-suite of Palantir offerings are considerably more extensive. The S-1 includes 18 product screenshots (rare for a filing) but perhaps unsurprising: the company is actively battling its profile as a "services" firm. Here's a look at the sprawl of Gotham and Foundry:

A selection of Gotham products, Palantir’s S-1 filing

A selection of Foundry products, Palantir’s S-1 filing

The sheer volume of product built is impressive, even if they've been at it for 17 years. They've also assembled an extraordinarily comprehensive data stack that, in sum, competes with popular commercial alternatives like Tableau, Alteryx, Google Sheets, Retool, Typeform, TimescaleDB, Snowflake, Airflow, Flink, Kafka, Jupyter, Databricks. That's without mentioning the hardware products on offer.

Below, we discuss a few critical pieces of the Palantir puzzle, including its integration work, knowledge graph, and GUIs. We unpack what Palantir's product offering tells us about who they are as a company, and early network effects.

Integration

One of the lessons upon which Palantir's business relies is that humans are the real bottleneck when it comes to data. The government agencies the company serves already store enormous amounts of information, but humans need the right tools to extract insights. Consequently, Palantir's first challenge is integration with existing storage and software systems. The company is keen to express the importance of working alongside legacy systems rather than forcing customers to rip and replace them. It's worth noting that integrating with those systems is notoriously challenging. Entire companies, like Fivetran, have been built around integrating with more modern architectures. While committing to work with these systems is almost certainly a necessary part of the firm's sales pitch (customers don't want to be told they have to lose pieces they find valuable), it's a decidedly non-trivial project.

Knowledge graph

Once integrated, Palantir's infrastructure enables users to define their own, intuitive ontologies and navigate a "knowledge graph," the same type of architecture that Google uses to link concepts and entities on the web. Again, as is the case with integrations, there is an entire class of companies dedicated to knowledge graphs (i.e., Neo4j, Tigergraph, Stardog).

GUIs

Remember the fallible human? To address their frailties, Palantir has built an array of GUIs to help application developers, data analysts, and operators interact with, query, and build analysis and products with big data. Below is a summary table of these products, with comparable commercial offerings for reference:

Other products

In addition to the products above, Palantir has built a range of other solutions. This includes a proprietary time-series database, a novel compression system, a native data lineage platform, a suite of ML Ops tools (including explainability, model versioning, and more), and compliance solutions. Each of these alone represents an entire market. It's worth mentioning these more to enunciate the sheer range at play here, though, beyond a breathless list, there's not a huge amount to be gleaned.

Consultancy or software company?

There are multiple ways to interpret the Gotham and Foundry bundles. Either Palantir's bespoke R&D model enables them to develop good-enough solutions in all of these challenging areas, which they are then able to bring to their full customer base, or they've had to create unique solutions for each customer. The former sounds like a customer-led software company, the latter like a services business.

It's possible the "Forward Deployed Engineer" strategy Palantir uses (they require engineers to spend time directly interacting with customers) has enabled them to uncover product needs quickly and build integrations faster than competitors.

On the other hand, perhaps each of these modules was developed with only one or two customers in mind and is not broadly used. How many of their government customers use Ava, for example? How many of their commercial customers use Fusion and Quiver? It's hard to parse.

Network effects

Palantir lists "generate network effects" as one of the foundational tenets of their approach to building technology.

The first level of network effect exists within a product. As Palantir opens up data access via deep integrations, more application developers come in to build custom apps, which increases demand for other data products, pushing developer activity into new use cases. They reference a financial services customer where the platform scaled from one use case to more than seventy across compliance, front office, risk, and internal audit desks.

The next level of network effects exists between customers. Palantir argues the lessons from deploying their platforms in one account are incorporated back into the product, for all. It's hard to judge the legitimacy of this network effect in the governmental context. Certainly, some local police departments will have similarities and can benefit from the same product enhancements, but across all customers, how common are integrations, pain points, and operational needs? The case is more robust for Foundry within a given commercial segment. In aviation, Palantir has built a shared data platform for more than 100 airlines and 15 suppliers, in partnership with Airbus. This is a true network effect: the more nodes that join, the more valuable the network becomes. Palantir notes that they're working on similar initiatives in healthcare, automotive, and "government sectors." If executed correctly, this would significantly strengthen the network effects narrative.

Business model

Palantir may be confusing to different stakeholders, but its business model is far easier to grasp from an investor's standpoint. The company is also a case study in the power of a healthy procurement process, especially for enterprise sales cycles.

Think of Palantir's business model as one part software (Gotham and Foundry) and one part consulting firm. The software business drives long, recurring relationships with customers at high margins. Contracts also expand as time passes. The consulting firm deploys staff to a customer's premise, ensures value is extracted and upsells more software. Palantir describes this virtual cycle as the "Acquire, Expand, and Scale" approach.

Let's go deeper into each.

Acquire

Palantir spends a considerable amount of time in the S-1 detailing their go-to-market. For an average customer to pay $5.6M a year, Palantir has to do a lot of work. Often, this results in a loss, both in terms of cost and a time-sink. Palantir needs to go through a time-intensive, multi-level approval matrix and budget-constrained purchase consideration for a buyer to procure software. It may be the most demanding enterprise software sale we've ever analyzed. It's common for software pilots to take six months (on the low end) and a year or more to convert into a full paying customer. Over time, Palantir looks to extract more revenue as usage increases.

Customers in the Acquire phase typically spend $100K in the first year of using Palantir's offering. That's a paltry sum for a considerable amount of work, but Palantir is happy to play the long game with the knowledge that future riches will reward their efforts.

To understand how clients graduate from a $100K pilot to an annual fee of $5.6M (59x in yearly contract value growth), you need to focus on CEO Alex Karp and the 250 days he spends on the road each year.

Expand

You read that right. Pre-COVID, Alex Karp traveled ~70% of the year.

Why? To close sales. His presence is required to win and mature contracts, fundamentally altering a customer account's underlying profitability. Of course, he is aided by staff and other members of a sales team. But his calendar is an indication of how critical he is to these conversations. (Incidentally, sales makes up just 3% of headcount.)

This is an interesting difference from other enterprise software companies. In many organizations, an EVP or SVP of Sales is the best-compensated person in an organization, prized because of their ability to convert customers. Palantir is a genuine outlier and nearly impossible to replicate, given the reliance on the CEO's attention and time.

Scale

Palantir's unit economics change during the Scale phase. From the filing (emphasis ours):

As customer accounts mature, our investment costs relative to revenue generally decrease, while the value our software provides to our customer increases, often significantly, as usage of the platform increases across the customer's operations. In this third phase, after having installed and configured the software across an entire enterprise, customers become more self-sufficient in their use of our platforms, including developing software and applications that run on top of our platforms, while still continuing to benefit from the support of our operations and maintenance ("O&M") services.

It is in the Scale phase of our partnerships with customers that we generally see contribution margin on particular accounts improve. In 2019, we generated $565.7 million in revenue from customers in the Scale phase, with a contribution margin of 55%. In H1 2020, those same customers generated $296.3 million in revenue, with a contribution margin of 68%.

As customers get to grips with Palantir's tools, they require less hand-holding. At the same time, usage tends to increase, resulting in larger contracts with significantly less effort.

Moreover, given that Palantir's customers are often a government body, limits on annual contract value (ACV) may not exist. There aren't the same requirements to balance the books at the Department of Defense. An illustrative chart indicating Palantir's room to grow within government:

Palantir’s S-1 filing

Palantir's mechanics of a customer sale is a fascinating example of a strong procurement strategy and a real narrative violation: selling to the government in a long, arduous process can turn out to be a very lucrative business model.

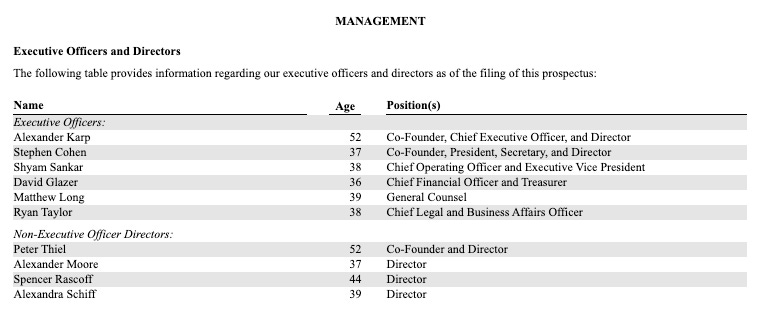

Management team

In many ways, Palantir's management team of Peter Thiel, Alex Karp, and Stephen Cohen reflect ringleader Peter Thiel's contrarian disposition. All three were vital architects and defendants of Palantir's strategy to develop a controversial line of surveillance products and work with government customers that make other technology companies hesitate. This willingness to do what others won't is not merely in each of these executives' DNA—it's a key to their success. Understanding why Palantir's management operates this way begins by understanding Peter Thiel.

Palantir’s S-1 filing

Peter Thiel

By now, Thiel's story is well known. After brief stints as a lawyer and a securities trader, Thiel left corporate America to start an online payment company named Confinity. Thiel would eventually merge Confinity with Elon Musk's online banking company, X.com, to form PayPal. Thiel and Musk grew PayPal into one of the dotcom era's biggest success stories, eventually selling to eBay for $1.5B, as mentioned. Thiel parlayed his successful exit from PayPal into a string of enormously successful endeavors in the technology industry. From becoming the first outside investor in Facebook to backing Airbnb, Stripe, and Spotify through his VC firm Founders Fund, Thiel has been involved with some of the most significant technology companies in the last two decades.

In addition to his professional successes, Peter Thiel has spent significant time and money evangelizing his contrarian ideals. To address his belief that universities brainwash their students, he set up the Thiel Fellowship to give college students a $100K grant to drop out and pursue an idea of their choice. He was one of the very few Silicon Valley celebrities who supported Donald Trump in 2016 — even donating over $1 million to Trump after the notorious Access Hollywood tape emerged. (He finally broke with Trump over his disgust at how badly Trump handled COVID-19. But before he did, Buzzfeed reported he met with white supremacists who support Trump.) Thiel has even spent significant resources to promote the development of floating cities that will run under libertarian-leaning governments and use cryptocurrencies.

Given all this, it shouldn't surprise that Thiel chose a non-conventional route when it came time to build the Palantir team.

Alex Karp

Take CEO Alex Karp. Unlike most tech CEOs, Karp is neither an engineer nor an MBA. Nor does he have much tech experience. In fact, before becoming Palantir's CEO, Karp had never worked at a technology company. Karp was a friend of Thiel's from Stanford Law School, who went on to earn a PhD in neoclassical social theory. Upon completing his PhD, Karp received an inheritance from his grandfather. He invested successfully enough to create the money management firm, Caedmon Group, which works with wealthy European families.

While Karp may have an odd background for a tech CEO, his raw intelligence, vision, and—not least—capacity to raise funding from wealthy donors made him attractive to Thiel. And, though they approached the world from vastly different political perspectives (Thiel, the libertarian; Karp, the socialist), Karp embraced Thiel's aversion to Silicon Valley mores. Karp chose to work primarily from a one-room barn in New Hampshire. Recently, he moved Palantir's headquarters to Denver. In sum, Karp has consciously distanced himself—and Palantir—from the rest of Silicon Valley, not just in the physical sense. Under Karp, Palantir has continued to develop technology tools for the US Defense Department (DoD) and Immigration and Customs Enforcement (ICE), even in the face of Palantir employee protests. By contrast, Alphabet has withdrawn its involvement in the DoD's use of its artificial intelligence to assist in drone strikes. Karp has pointedly refused.

Whether you agree with his stances or not, Karp's willingness to vigorously defend its choices will be vital for Palantir as it encounters increased political and social scrutiny upon going public.

Stephen Cohen

Rounding out the Palantir management triumvirate is president and co-founder Stephen Cohen. As a Bay Area native and Stanford computer science graduate, on the surface, Cohen appears to be more of a traditional tech executive than Thiel or Karp. But he has worked alongside Thiel for his entire career and embraced many of Thiel's perspectives.

The pair's relationship began at university, with Cohen serving as editor-in-chief of The Stanford Review, a right-wing newspaper started by Thiel. Cohen then worked with Thiel at Clarium Capital — Thiel's ill-fated investing venture — as an intern. Shortly after, Cohen helped Thiel develop Palantir's initial prototype.

Since then, Cohen's developed a reputation for getting things done, scaling Palantir's product and operations. He is reported to have earned the moniker "Mr. Two Weeks" from the CIA because of his ability to steer teams to turn around product releases quickly. Within the Palantir leadership team, Cohen has retained this reputation as a "doer" and will be crucial in executing Thiel and Karp's bold and unique vision.

Maintaining control

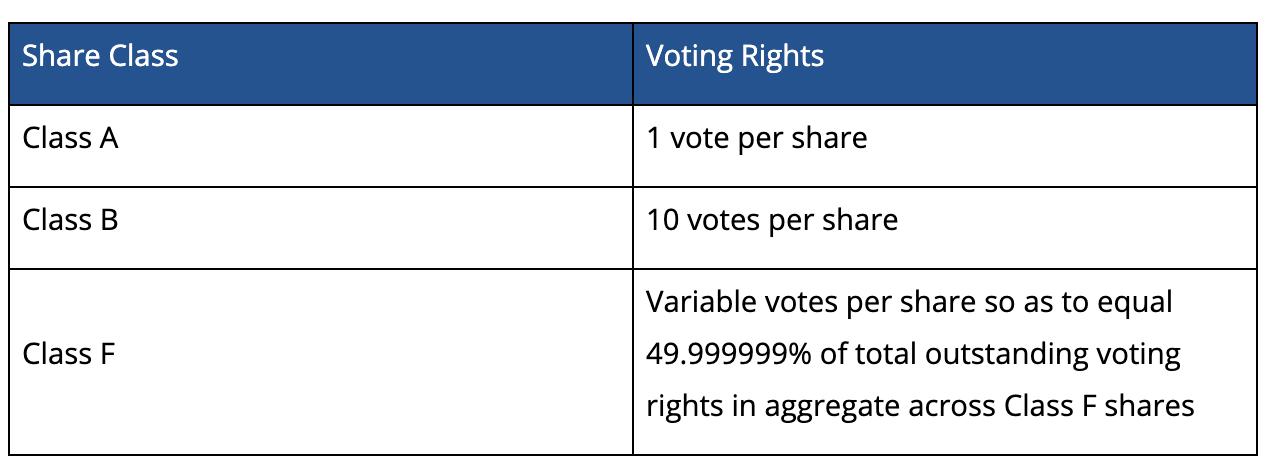

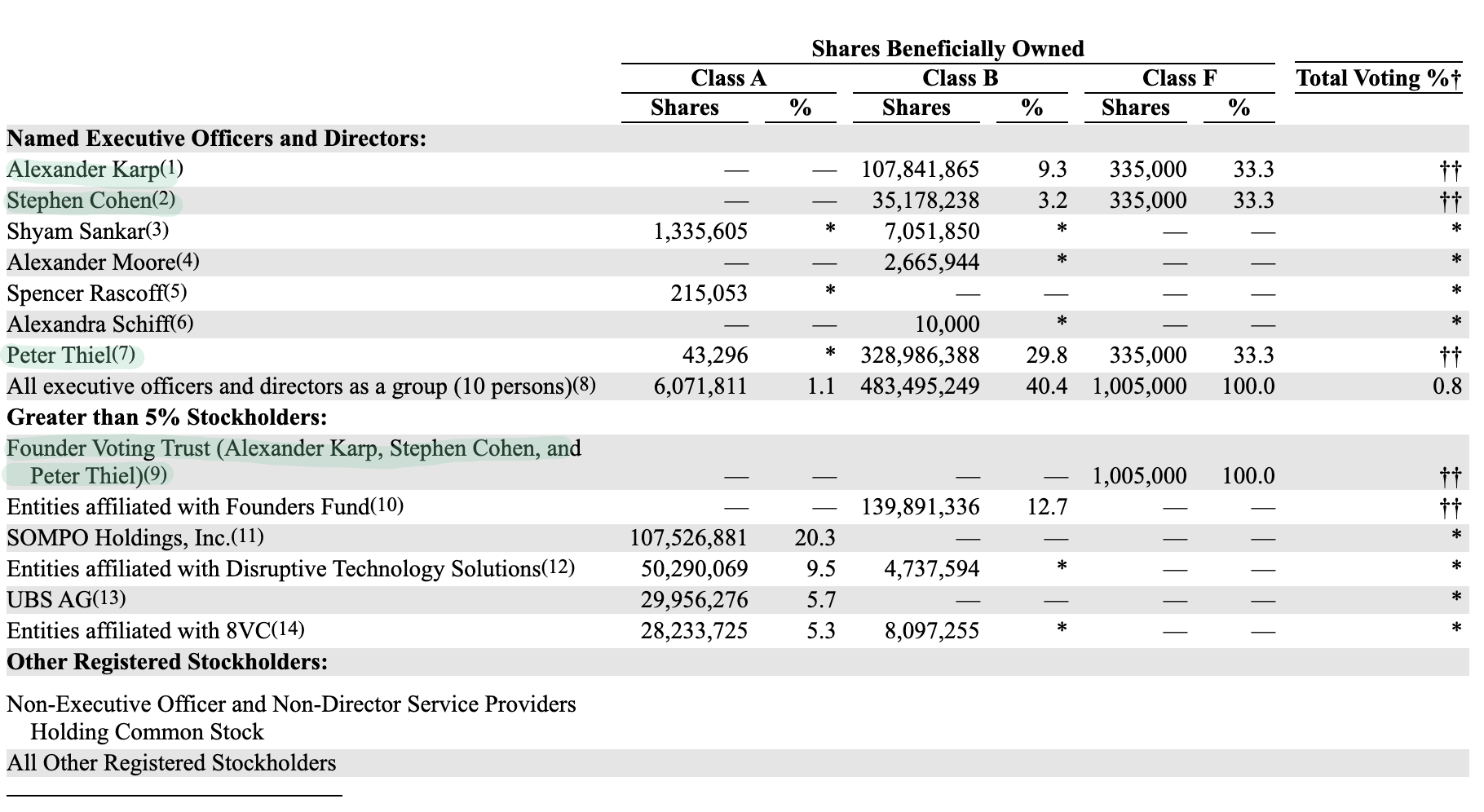

One of the most interesting — and commented-upon — findings within the S-1 is how Thiel, Karp, and Cohen have created a new take on multi-class equity structures to retain voting control. This has been achieved through the creation of a new class of shares owned by the three founders. This "Class F" totals 49.999999% of all votes regardless of the number of shares outstanding. This will allow Thiel, Karp, and Cohen to retain control of Palantir.

Multi-class equity structures are not new. For years, companies have offered investors access to different classes of shares that have different voting rights. For instance, Pinterest has two classes of shares: Class A shares, which are entitled to 1 vote per share, and Class B shares, which are entitled to 20 votes per share. When Pinterest went public, it issued its leadership team and key investors Class B shares while giving Class A shares to everyone else. This allowed the leadership team and key investors to maintain a voting majority even if they are a minority equity holder.

Palantir's Class F structure pushes the concept further. The equity structure looks like this:

Palantir’s S-1 filing

With possession of the Class F holdings alone, the co-founders have almost majority control. Given that the trio also holds significant portions of Class A and B shares, there should be no mistaking who's in command of this ship. Thiel directly holds 29.8% of the available Class B shares, along with an additional 12.7% through Founders Fund. Karp and Cohen hold 9.3% and 3.2%, respectively.

Palantir’s S-1 filing

The three co-founders have also signed what they call the "Founders Voting Agreement." In it, Thiel, Karp, and Cohen have decided that all of their combined votes will be cast in a manner agreed upon by the majority of the three. This agreement ensures that the team will maintain power until they choose not to.

This may seem like another attempt by a group of tech founders to retain control of their creation. In reality, it's more significant. This equity structure is crucial to enabling the business strategy and management style of the founding team. As we previously mentioned, Thiel, Karp, and Cohen have built Palantir's success by being contrarian — by making unpopular decisions, taking unpopular stances, and sticking to them in the face of intense public scrutiny. This equity structure will give the three founders the breathing room necessary to take bold risks without the fear of being replaced. This structure allows Karp to tell investors "to pick a different company" if investors don't like how they do business.

Investors

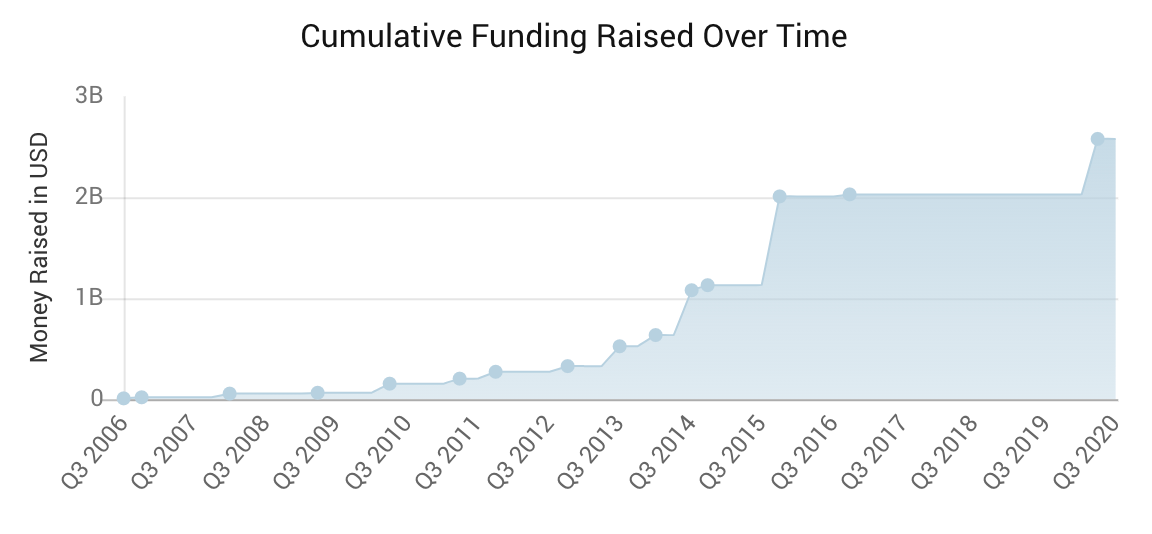

Palantir's path to an IPO has been an interesting one. They raised a total of $2.6B, including a $500M round in June from Sompo Holdings.

That recent round means that Palantir does not need capital as it goes public and has enabled them to choose a Direct Listing. That means the company is not issuing new shares but enabling existing investors and shareholders to directly sell to the public.

Crunchbase

Before the Sompo round, Palantir last raised in 2015. That $880M round pegged the company at $20B. Given the company expects a similar valuation in the public markets five years later, it's safe to say that Palantir isn't a breakout investment for the later stage investors. Earlier investors should do well.

The big shareholders in Palantir include familiar Silicon Valley names. As noted, Peter Thiel's Founders Fund owns ~12%, while Joe Lonsdale's 8VC owns ~5%. Less familiar names include Sompo. The Japanese insurance firm holds ~20% and operates a joint-entity with Palantir in their home country. Entities associated with Disruptive Technology Solutions own 9.5%, and UBS owns 5.7%.

It's worth considering what the success of Palantir might mean for investor interest. Historically, governments and the defense sector clients have been viewed as demanding, esoteric customers, tricky to win. Startups with ambitions in the space have been viewed with skepticism. Palantir may change that. The viability of their model and the magnitude of their win could soften the stance of venture capitalists.

Anduril, founded in 2017 and focused on national and border security, has been backed to the tune of $241M by Founders Fund and General Catalyst. They may be the start of a larger second wave.

Financial highlights

The financial debate about Palantir is over their long-term economics. Are they a consulting company that hires workers at one wage and shops them to clients at higher prices? If so, they should trade in line with companies like Accenture and IBM, whose investors don't view their businesses as especially scalable. Or are they an enterprise software company that spends money upfront to lock in long-term clients, and then earns high incremental margins as those clients keep renewing and upgrading their services?

We'll review the company's revenue, margin structure, customer concentration with an eye on the question. We'll also alight on a rather esoteric source of financial growth.

Reasonable revenue growth

As detailed in "Palantir's History," the company has been around for some time. Palantir shares revenue figures from as far back as 2008, through the first half of 2020 (1H20).

Growth has been solid, if unspectacular, in recent years. Revenue grew 10% from 2016 to 2017, 15.5% from 2017 to 2018, and 24.8% between 2018 to 2019. There's been a meaningful uptick in 1H20, with revenue over the first six months reaching $481.2M, a 49% increase year-over-year (YoY).

Palantir’s S-1 filing

This may be partially attributable to the coronavirus outbreak. From the S-1:

The pandemic has made clear to many customers that accommodating the extended timelines ordinarily required to realize results from implementing new software solutions is not an option during a crisis. As a result, customers are increasingly adopting our software, which can be ready in days, over internal software development efforts, which may take months or years.

For a company that seems to thrive from disarray, Palantir may find the second half of the year just as profitable should we see an uptick in cases.

Expected customer concentration

If your focus is governmental agencies and large corporates, a certain customer concentration is expected. Palantir has a grand total of 125 customers, spanning 36 industries and more than 150 countries.

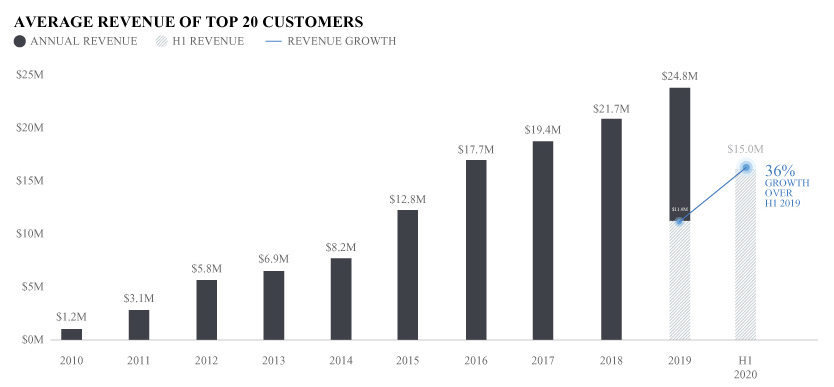

Even within that small cohort, Palantir relies on a subsection for the majority of its revenue. The company's top twenty customers represented 67% of 2019's revenue, a total of $495.2M. The top client represented 15% of revenue in 2018, 12% in 2019, and 11% in 1H20. Another company represented 10%. Since 2010, Palantir has expanded the ACV of its top twenty customers from $1.2M to $24.8M in 2019.

Palantir’s S-1 filing

Among this cohort, the average lifespan is 6.6 years.

Modulating margins

We discussed the three customer phases under "Business model." As alluded to, each has different margin profiles.

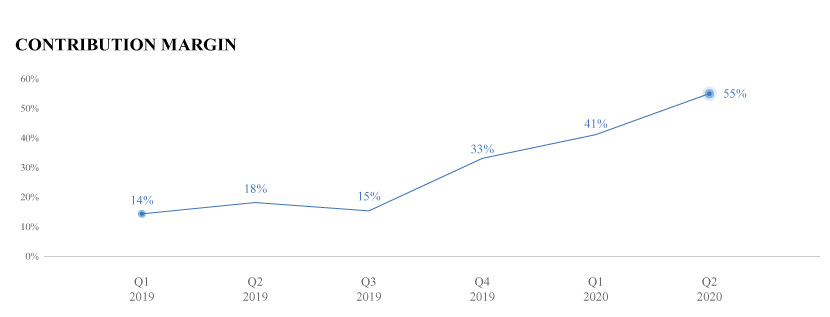

During "Acquire," Palantir bears the cost of customer acquisition. In 2019, the company earned $0.6M in revenue and lost $65.4m in contribution profits from customers in this phase. Costs include selling and the process of customizing software for use.

In the "Expand" phase, margins remain low. In 2019, customers in this phase generated $176.3M in revenue with a -43% contribution margin. These customers become profitable in time: in 1H20, 2019's expansion cohort generated revenue of $160.5M, for an 82% increase in annual run-rate. The contribution margin for this period was 35%.

Finally, in "Scale," Palantir's plan comes into its own. These mature customers make up most revenue, generating $565.7M in 2019, with a 55% contribution margin. These margins are high in part because Palantir defines these customers based on an annual spending threshold and positive contribution profits. That said, the size of the group indicates that Palantir can scale some customer relationships. Furthermore, Palantir says that its largest customers generate higher contribution margins, with the biggest pegged in the high 80s.

Palantir’s S-1 filing

A further note: contribution margins are nice, but not if they require high fixed costs. Palantir does have high non-client-related expenses. G&A alone was $320.9M in 2019, 43% of revenue. Palantir has cut down on expenses of late, reducing employee perks and limiting travel due to the pandemic. Still, the business is at a paradoxical stage—its size implies that it is relatively mature. However, the slow cadence of unit revenue growth implies that they're still in a low-margin phase of existence.

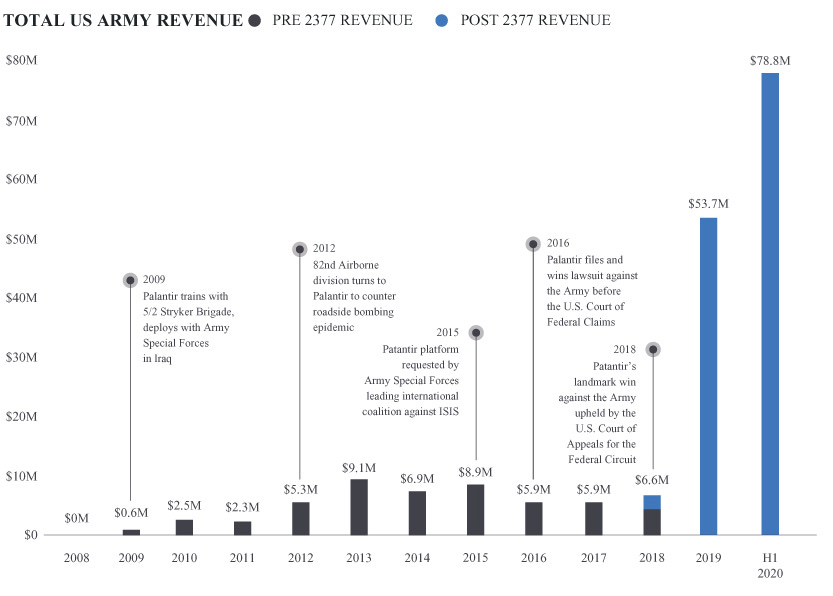

Palantir v. the United States

To win business, Palantir is willing to go to extreme lengths.

One anecdote: in 1994, Section 2377 of the Federal Acquisition Streamlining Act (FASA) was passed. This required the US federal government to consider commercially available software to fulfill its needs, rather than hiring contracts to create something bespoke.

The law was largely ignored until 2016, when Palantir won a suit against the US Army, challenging the decision to pursue a custom-built solution for its "battlefield intelligence system." The decision was upheld by the US Court of Appeals, paving the way for increasingly large contracts for Palantir.

Palantir’s S-1 filing

In 2019, Palantir was reported to have bested Raytheon for an $800M contract with the Army.

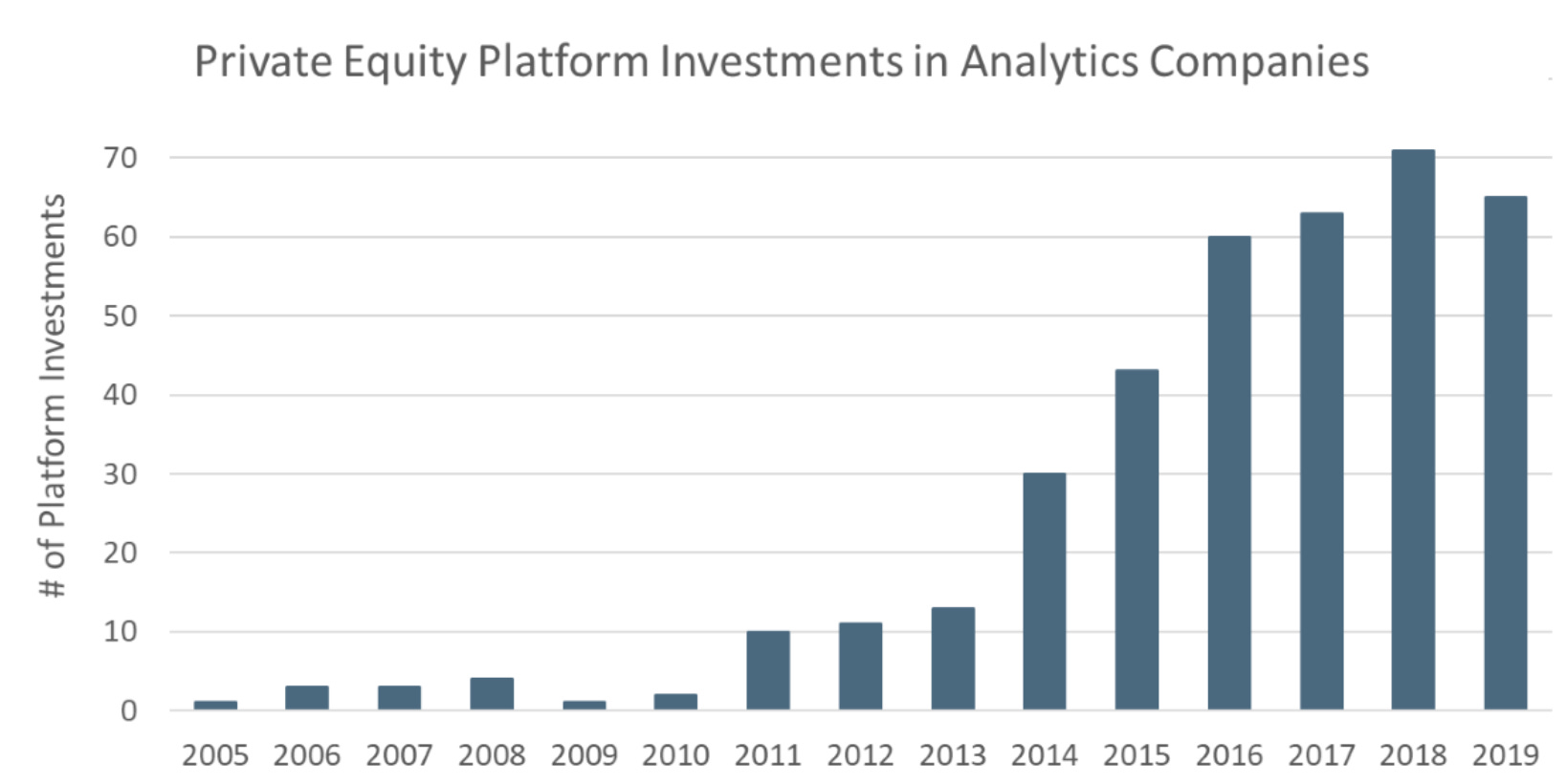

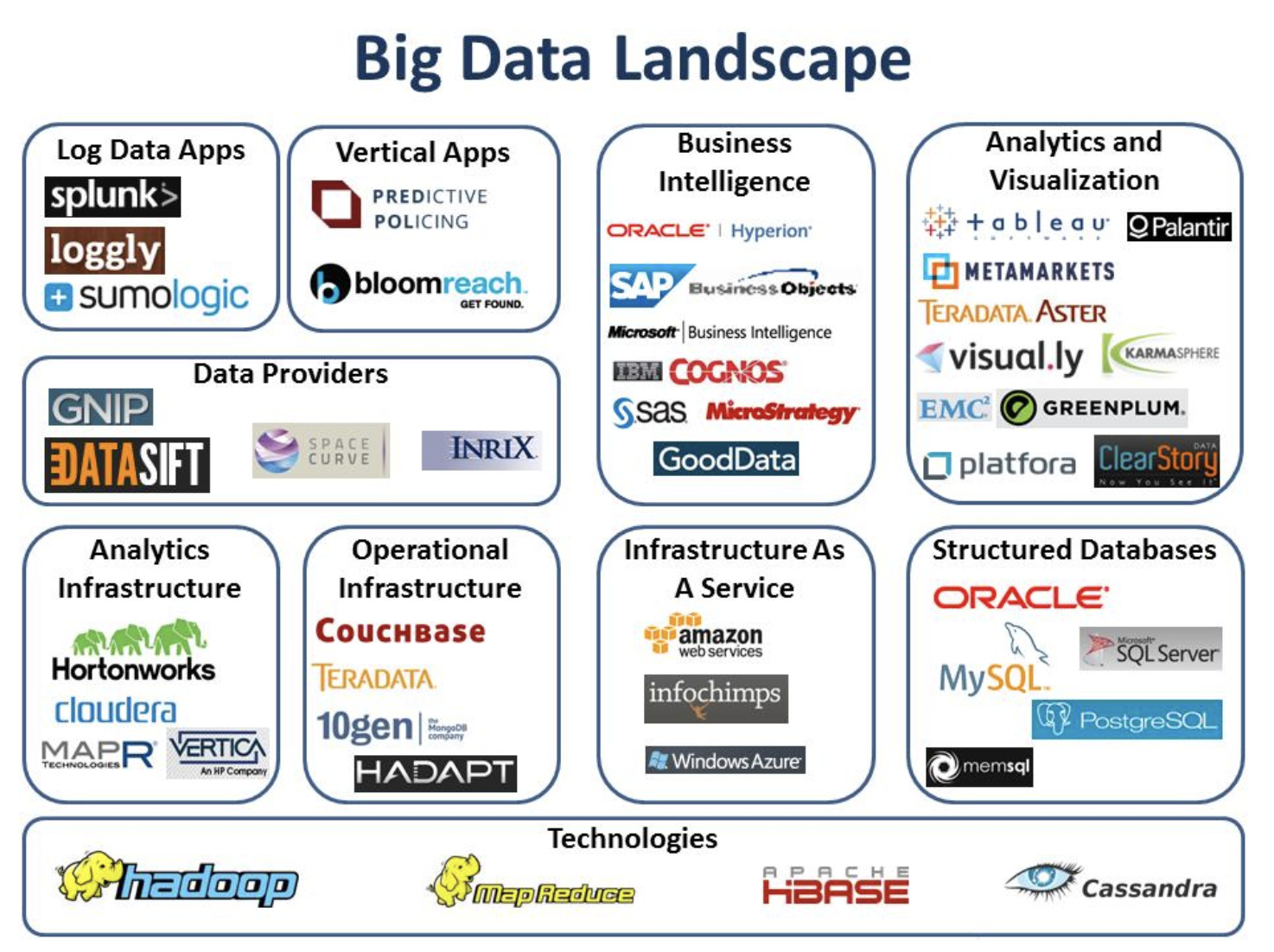

Competition

Though Palantir historically benefited from relatively little competition following its founding in 2003, times are changing'. Private investment in the analytics space has boomed since the financial crisis.

Private Equity Info

Today, big data and information management platforms are spread deeply across most verticals. As the landscape below shows, the Analytics and Business Intelligence sectors are littered with startups and incumbents alike.

Analytic Bridge

As we've discussed, Palantir is a business with two-faces: software company and consultancy.

As a software company, Palantir faces stiff competition from incumbents, like Alteryx, IBM Watson Studio, and Tableau. They also battle startups, including DataVisor, Digital Shadows, and Seeq. This is far from an exhaustive list.

As a services firm, Palantir competes with tech-forward consultancies, principally Accenture, IBM, McKinsey, Bain, and BCG. Though the big four consultants tend to focus more on strategic, operational, and growth advice, there has been a push to expand in-house analytics capability. Notably, McKinsey acquired QuantumBlack in 2015 to bolster its data offering.

As data becomes more accessible, and cloud computing more powerful, analytics and ML models are becoming increasingly commoditized. Pure software vendors may find it challenging to compete in this crowded environment, while consultancies will always have comparatively depressed margins. In this respect, Palantir benefits from its dual software/services business model. Relative to pure software providers, Palantir can customize their offering and wrap a service layer around it. Compared to consultancies, Palantir boasts significantly more robust tooling. As discussed, over time, this can boost the company's margin profile.

Ethical dilemmas

Palantir is unlike any other Valley company and may be one of the most idiosyncratic public companies of all time. While the company's founding story, product, or financial profile might generate excitement by themselves, the political and ethical issues raised earlier make it particularly fascinating. Shareholders may be interested to understand better the stances and controversies that define the business.

Critical of Big Tech

The liberal persona of Silicon Valley is the antithesis of Palantir as an idea, let alone a tangible company, and as alluded to, the company openly acknowledging this fact (emphasis ours):

Our company was founded in Silicon Valley. But we seem to share fewer and fewer of the technology sector's values and commitments.

From the start, we have repeatedly turned down opportunities to sell, collect, or mine data. Other technology companies, including some of the largest in the world, have built their entire businesses on doing just that.

Software projects with our nation's defense and intelligence agencies, whose missions are to keep us safe, have become controversial, while companies built on advertising dollars are commonplace. For many consumer internet companies, our thoughts and inclinations, behaviors and browsing habits, are the product for sale. The slogans and marketing of many of the Valley's largest technology firms attempt to obscure this simple fact.

The world's largest consumer internet companies have never had greater access to the most intimate aspects of our lives. And the advance of their technologies has outpaced the development of the forms of political control that are capable of governing their use.

The bargain between the public and the technology sector has for the most part been consensual, in that the value of the products and services available seemed to outweigh the invasions of privacy that enabled their rise.

Americans will remain tolerant of the idiosyncrasies and excesses of the Valley only to the extent that technology companies are building something substantial that serves the public interest. The corporate form itself — that is, the privilege to engage in private enterprise — is a product of the state and would not exist without it.

In its declamation and positioning, Palantir is explicitly in opposition to Facebook, Google, and other companies in that cohort.

Modest gains under Trump

As you may know, Peter Thiel is an outspoken supporter of Trump and despises the Valley's lack of progress in the last 30 years. Karp dislikes Trump but has been supportive of Palantir's relationship with ICE and the Pentagon even after the likes of Google and Amazon abandoned their contract. From a NYT piece:

"Mr. Karp, whose parents met at a civil rights demonstration, said he believed that American companies, including those in Silicon Valley, had a moral obligation to support the country and its military, no matter who was living at 1600 Pennsylvania Avenue

"We're proud that we're working with the US government," he said."

With that in mind, you might assume the Trump presidency has been beneficial for a company that mostly sells into the US Federal Government. You'd be wrong. The company's revenue grew, on average, 145% in the Obama administration compared to just 17% in the last three years. There is an element of absolute scale here — it's easier to 5x from $2M than it is from $200M — but the sharp decline is still eye-opening and something of a surprise for a company inextricably linked with the administration's enforcement of American borders.

ICE

Palantir stops short of naming ICE. There's more than a passing reference to it, though. Under "Risk Factors," the company describes targeting from "activists" and subsequent negative press (emphasis ours):

Our relationships with government customers and customers that are engaged in certain sensitive industries, including organizations whose products or activities are or are perceived to be harmful, has resulted in public criticism, including from political and social activists, and unfavorable coverage in the media. Activists have also engaged in public protests at our properties. Activist criticism of our relationships with customers could potentially engender dissatisfaction among potential and existing customers, investors, and employees with how we address political and social concerns in our business activities. Conversely, being perceived as yielding to activism targeted at certain customers could damage our relationships with certain customers, including governments and government agencies with which we do business, whose views may or may not be aligned with those of political and social activists.

At present, Palantir has two contracts with ICE, potentially worth as much as $92M. In serving the agency, Palantir's software has been used in operations to apprehend dangerous criminals. In 2011, the company's services were used in the successful "Operation Fallen Hero," which focused on the Los Zetas drug trafficking ring.

As noted in "Palantir's History," recent years have seen the company's software used to keep tabs on those suspected of breaking immigration laws. This is particularly true when referring to Palantir's Investigative Case Management (ICM) system — a database to track information on an individual. In at least once instance, the ICM was used to target the parents of migrant children. If parents were found to have assisted in bringing their children across the border, they could be arrested and deported. Helping ICE separate families has prompted consternation from civil rights groups and those closer to home.

A group of employees expressed displeasure with management over the ICE contracts. To date, the Palantir has held firm even as Google and Microsoft have retreated from equivalent engagements.

Playing favorites in geo-politics

Palantir's dedication to the American way of life creates interesting constraints on the company's realistic TAM. With 60% of the company's 2019 revenue coming from outside of The United States, there is a constant reckoning happening within the company walls. Yes, The UK, France, and most of Europe follow similar liberal, democratic principles that America does. Still, the other 34% of revenue falls into countries that may, or may not, fall in line with America's policies in the future. These different geographies are also the second-fastest-growing segment behind the States. Palantir does not disclose any specific customer names, so it is unclear whether ROW customers are predominantly corporates or government.

We estimate the TAM in the government sector, including government agencies in the United States, its allies, and in other countries abroad whose values align with liberal democracies, is $63 billion."

The company is open in its dismissal of China. Under "Risk Factors," the firm notes that China presents a potentially lucrative market, but serving the nation would be inconsistent with the firm's values.

Our leadership believes that working with the Chinese communist party is inconsistent with our culture and mission. We do not consider any sales opportunities with the Chinese communist party, do not host our platforms in China, and impose limitations on access to our platforms in China in order to protect our intellectual property, to promote respect for and defend privacy and civil liberties protections, and to promote data security.

In the future, Palantir may face a reckoning. Global policy and allies change at an increasing speed, and the company will have to be nimble in understanding who they are arming. It's worth noting that a potential new administration will also add a layer of risk for investors — it's unknown what Biden's stance will be on non-government companies acting as the arms dealer for governments worldwide.

Why now?

The easy answer? Look at the market. Approaching all-time highs make an attractive entry point. Add a "SaaS" industry tag on top of that broader market success, and you're likely a nice opening price.

Compared to some of the other recent debutants, Palantir's choice of timing may have more to do with politics. November's election is far from decided, and given the importance of government backing, the company may have wished to enter the public markets before a potential change in administration. Given the growth seen during Obama's tenure, a Biden win is far from a death knell, though it does represent more of an unknown.

There is also something of a growth story for the company to tell at the moment. As mentioned, 1H20 revenue grew 49% YoY compared to 15% from 2017 to 2018 and 25% from 2018 to 2019. That narrative may not hold for the latter half of 2020 and beyond.

Finally, there may be few options left for the business. While the company raised earlier this year, it's unclear whether further venture funding is forthcoming. Given the IPO is expected to price below the last round of funding, we assume more generous private capital was not available. It will be up to Thiel and Karp to prove the wisdom of this latest move.

If you enjoyed our analysis, we’d very much appreciate you sharing with a friend. We’d also love to have you join us for today’s event.