Goldman Sachs: The Quest for Eternal Youth

The firm has spent billions attempting to transform itself into a tech company, exploring lending, savings, investing, and beyond. The initiative shows the opportunities and challenges of innovating.

Actionable insights

If you only have a few minutes to spare, here's what investors, operators, and founders should know about Goldman Sachs’ tech efforts.

A pivotal moment. Goldman’s investment in technology has come under increasing pressure. The firm’s price-to-book value lags competitors like Morgan Stanley. Some have argued that Goldman’s heavy investments in technology have dragged down its stock price.

The impact of the financial crisis. The roots of Goldman’s consumer tech efforts can be traced back to the 2008 financial crisis. To survive, the firm turned itself from an investment bank into a bank holding company. Though this shift came with new responsibilities, it also opened the door to different products.

The cost of consumers. The high-level figures suggest Goldman has succeeded in building a meaningful consumer business. It boasts 14 million users with $110 billion in deposits, interacting with a range of products. Such growth has come at a cost.

Becoming a platform. Goldman’s most promising tech initiatives treat the firm as a platform for others to build upon. Its Transaction Banking (TxB) service seems to be growing rapidly with this approach.

The challenge of cultural change. Succeeding as a builder of technology has required Goldman to change its culture. Though it has made headway attracting engineering talent, it still has a way to go.

Banks are the tortoises of the business world. Through war and peace, poverty and prosperity, stagnation and innovation, financial institutions survive. Not all, of course – only the lucky, hardy few. But those that do can live to a ripe old age. Consider Banca Monte Dei Paschi di Siena, founded in 1472, in time for a twenty-year-old Leonardo da Vinci to solicit its services should he have found himself fifty miles south of Florence. Despite being more than half a millennia old, “BMPS” still counts nearly 4 million customers and a few billion euros in revenue.

By those standards, Goldman Sachs is a fresh-faced adolescent. Founded by former shopkeeper Marcus Goldman in 1869, the eponymous bank has developed into one of the world’s mightiest countinghouses. By assets under management, its $1.2 trillion is enough to rank fifth in the U.S., behind only JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo. Net revenue totaled $59.34 billion in 2021.

Nature tends toward decay, however. Though Goldman may seem in reasonable health, it cannot expect to maintain it without effort. As Jeff Bezos wrote in his final annual letter, “Staving off death is a thing you have to work at.”

To its credit, Goldman recognized its mortality earlier than many of its peers. In 2014, the Manhattan-based firm started investing heavily in technology, mindful of its disruptive power. In the years since, it has built out a suite of consumer and enterprise tech products spanning savings, lending, credit, and transaction banking. In the process, it has allied itself with modern trailblazers like Apple and Stripe.

At first glance, such initiatives appear impressive – a sign of positive momentum, rejuvenation in motion. A closer look, however, encourages a more cautious appraisal. While Goldman has successfully shipped fintech products, it's unclear whether they have repaid the firm’s effort and investment. The result is a storied institution that seems stalled between its past and future, with pressure rising. Goldman is estimated to have spent $5 billion on its consumer banking efforts, an expense many believe has dragged down its stock price. With earnings potentially dropping as much as 35% this year, such profligacy is under fire.

In today’s piece, we’ll discuss:

Catalysts. What led Goldman to embrace technology – particularly products geared toward consumers? The answer involves the financial crisis, Occupy Wall Street, and the advent of fintech.

Goldman’s tech efforts. Of its digital products, the bank is best-known for its high-earning savings account. As it turns out, Goldman has built many other products, including those geared towards the enterprise.

The return on investment. Have Goldman’s tech initiatives produced the desired results? Amidst disappointments, there are also signs of promise.

Where next? If Goldman is to successfully transform into a tech business, it will need to make adjustments across its product suite. That may entail downsizing existing efforts and changing its culture.

Catalysts

Goldman Sachs is an unlikely consumer fintech company. Indeed, had you asked a partner in the year 2000 whether the firm would be offering personal loans to middle-class Americans a decade and a half later, they might have laughed in your face, throwing in an expletive for good measure. Such derision would not have arisen from uncertainty over Goldman’s ability to innovate. Much of the firm’s history had been marked by invention, with enterprising managers introducing new services over time.

No, the disagreement would have stemmed from the target customer. Since its founding, Goldman Sachs had risen to become arguably the most prestigious investment bank in the world. It served titans of industry and the businesses they ran. Few names commanded as much respect nor conveyed such power. The idea that so elite, so storied a shop would have deigned to provide $5,000 in credit to an insurance agent in Iowa or shopkeeper in Minnesota would have sounded ridiculous. Goldman operated in the world of billions and billionaires.

Time has a way of making the ridiculous seem reasonable. A series of global and industry shifts forced Goldman to change course so that by 2015, it was undertaking precisely the maneuver that would have prompted guffaws earlier in its life. Its evolution owed much to three catalysts: the global financial crisis, a changing industry, and an outmoded brand.

The financial crisis

Goldman Sachs escaped the global financial crisis of 2008 in better shape than most. Its survival and relative health owed something to its technological capabilities, as well as its managerial adaptability.

Unlike most firms, Goldman entered 2008 net short the mortgage market. It believed that mortgage-backed securities were worth much less than suggested and hoped to profit from their eventual decline. The firm was proven correct in that assessment – a call that proved lucrative but did not win it many friends on Wall Street. Goldman writing down these investments pressured the industry and helped catalyze its eventual implosion. In 2007, the firm made $4 billion from the short, with greater returns coming in 2009.

The shrewd read of Goldman’s team, especially Chief Risk Officer Craig Broderick, drove the firm’s hedge. But technology certainly helped. Securities Database, better known as “SecDB,” was founded by the firm in the early 1990s. Over the years, the software platform evolved to become a robust way for traders and risk management to track and model positions on a granular level. A senior source at the firm referred to the engineers that built it as geniuses. Another person with knowledge of Goldman’s history during this period noted it had been pivotal in profiting from the crash and navigating its fallout. Seeing tech act as a differentiator likely emboldened Goldman’s later efforts.

Reclassifying as a bank holding company was the more significant long-term shift. Coming into the crisis, Goldman was an investment bank. It benefited from fewer regulatory requirements, allowing it to borrow and invest more aggressively. While this model helped it (and rivals like Morgan Stanley) thrive for decades, it made it vulnerable during the meltdown. As distrust of this higher-risk style proliferated, clients fled, taking their money with them. To ensure survival, both Morgan Stanley and Goldman requested to become bank holding companies.

It represented a profound change. The benefits were obvious and immediate. Goldman could access the Federal Reserve’s lending facilities more flexibly and comprehensively as a bank holding company, giving it capital to weather the storm. A secondary benefit was that it inspired confidence in the market. Three days after it announced the change, Goldman raised $10 billion in equity, $5 billion of which came from Warren Buffett.

Though seemingly necessary, becoming a bank holding company came with drawbacks. By doing so, Goldman assented to much tighter regulation, diminishing its ability to take some of the risks it might have in the past. It also restricted the firm’s ability to take on debt and necessitated higher capital requirements.

At the time, the firm suggested the shift wouldn’t result in a change of strategy. With the benefit of hindsight, it clearly did. Without the ability to borrow as readily – or take the big swings that had delivered profits for so long – Goldman had to change its approach. Fundamentally, it had to learn to make money like JPMorgan Chase and Bank of America – large bank holding businesses. Instead of debt, these companies used customer deposits to secure funding.

As we’ll see, much of Goldman’s tech strategy has been geared toward attracting consumer interest and aggregating their capital.

A changing industry

In the aftermath of the crisis, tech began to survey the financial landscape and attempt to change it. In 2009, a neobank called Simple launched operations, becoming the first to do so in the U.S. Though not relevant to Goldman’s business at the time, the creation of products like Simple hinted at an accelerating trend: software was eating the world, and banking was on the menu.

Of particular interest to Goldman was the manner in which technology had the power to disintermediate gatekeepers. Much of the firm’s strength relied on its strong relationships. When a hedge fund manager wanted to make a trade, for example, they would call their connect at Goldman’s securities desk and place an order. Since these requests were not subject to an open bidding process, Goldman was able to ensure a healthy profit.

The advent of “multi-dealer platforms” challenged this position. Players like TradeWeb and MarketAxess allowed clients to surface their trades, opening them to multiple banks for bidding. The result for customers was usually a more economical option, with market competition driving down margins. One source suggested the industry’s direction of travel may result in trading revenues falling near zero. By 2014, Goldman was already feeling the pain of this change, with securities-trading income down 60% from 2009.

Technology was increasing transparency and disintermediation. If Goldman were to survive and thrive in the decades to come, it would need a more diversified, modern revenue base.

A bloodied brand

For much of its history, Goldman Sachs seems to have followed the maxim that it is better to be respected than liked. Its elite reputation helped it dominate in finance’s Gilded Age, even if it occasionally rubbed some the wrong way.

Starting in the aftermath of the financial crisis, becoming well-liked seemed more important to Goldman. The reputation of banks fell sharply during this period, with Goldman particularly affected. In a 2010 piece, Matt Taibbi memorably described the firm as “a great vampire squid wrapped around the face of humanity.” The Occupy Wall Street movement adopted the depiction the following year, with protesters marching a papier-mâché cephalopod up to the bank’s HQ. Another PR hit arrived in 2012 with a New York Times Op-Ed entitled “Why I Am Leaving Goldman Sachs,” which detailed cultural decay, going viral.

Like the SS officers in the famous Mitchell & Webb sketch, the relentless criticism and squid effigies seemed to prompt Goldman’s partners to ask themselves, “Are we the baddies?”

One source identified the need to humanize Goldman as a potential factor in its consumer efforts. Rather than being a fusty financial institution serving the uber-rich, Goldman could reframe itself as a tech-forward company bringing services to the everyman. As the respect the bank received from the public eroded, being liked may have felt increasingly important.

Embracing technology

As the story goes, it was during a 2014 off-site that Goldman made its first steps toward embracing consumer banking. After several years of sluggish revenue, the firm sought to reinvigorate itself. Rich Friedman, Head of Merchant Banking, suggested the organization take advantage of its bank holding company status to create new consumer financial products. CEO Lloyd Blankfein was intrigued. The “Project Mosaic” task force formed that same year to investigate the opportunity.

In the eight years since, Goldman has gone from tech curious to obsessed. And while its splashier consumer moves have generated the most attention, it has also devoted considerable resources to bolstering its enterprise offerings. Before assessing the success of Goldman’s tech push, we must first outline the extent of its initiatives.

Marcus

Most of the firm’s consumer efforts have occurred under the “Marcus by Goldman Sachs” brand. The name is a nod to the firm’s founder, Marcus Goldman. When presented to Lloyd Blankfein, he was reported to have said, “why didn’t I think of that?” Today, the unit divides its products into four categories:

Loans

Savings

Investments

Credit cards

In 2016, Marcus launched its first product: personal loans. Customers with credit card debt could refinance through the flexible, transparent service. Sources have suggested that Goldman picked that product after handling LendingClub’s 2014 IPO. Though the years have not been kind to the company’s market cap, the fintech was once a hot commodity, valued at nearly $9 billion. After seeing the business up close, Goldman’s team was convinced they could compete head to head.

Not all believe that was the right strategic move. One source remarked that Goldman entered the market several years too late, after competition had already developed. Moreover, the firm had chosen a product that tended to be a one-off interaction – customers refinanced credit card debt through Marcus and then left. If the goal was to create a sticky consumer business, a higher-frequency product like a credit card would have been more sensible. Nevertheless, Marcus’ loans have been well-received by consumers, with J.D. Power ranking it first by customer satisfaction.

Since launching, Marcus has tailored its loan product, targeting particular use cases, including home improvement, relocation, weddings, and travel. The home improvement category was bolstered by Goldman’s $2.24 billion acquisition of GreenSky. The Atlanta-based provider is “the largest fintech platform for home improvement consumer loan originations,” according to its CEO. The purchase brought GreenSky’s 10,000 merchants (that use the “buy now, pay later” product to streamline sales) into the fold. Marcus has also courted other merchants – partnering with both Amazon and Walmart to finance e-commerce sellers.

Savings seems to be Marcus’ most successful consumer product. The subsidiary offers high-yield savings accounts that generate between 1.90% and 2.70% per year. One source explained that enticing customers with such favorable rates makes sense for Goldman. Deposits represent a cheap source of funding for the bank, which it can then re-loan to generate revenue.

An acquisition boosted the assets under management of this product line. In 2015, Goldman purchased General Electric’s online deposit platform, which came with $16 billion in deposits and 140,000 customers. A few years later, Goldman rolled it into Marcus.

In February 2021, Goldman launched Marcus Invest. The robo-advisor manages a customer’s money across ETFs, rebalancing automatically. Clients can select different risk thresholds and choose between three themes, including one which focuses on meeting ESG criteria.

In collaboration with General Motors (GM), Marcus has created a line of credit cards. Customers of the “GM Rewards Card” earn 4x points on purchases and 7x on spending at General Motors. They can redeem accumulated points on GM vehicles and services. Beyond the classic rewards card, Marcus offers a version for businesses and those within GM’s “extended family,” including employees and suppliers.

Finally, Marcus offers financial literacy information and tools. Though not revenue-generating, products like the Marcus Insights app are designed to help customers keep track of their spending. Goldman’s $100 million purchase of Clarity Money formed the basis for this product. Though isolated from the rest of the Marcus suite at the moment, it could be a useful puzzle piece as Goldman attempts to create a cohesive banking experience.

Apple Card

Though Goldman has partnered with several tech giants, including Amazon and Stripe, its buzziest partnership is with Apple. In 2019, the pair released the Apple Card, a credit product designed for the iPhone. It takes no fees and supports multiple cardholders.

The product also secured an award from J.D. Power, topping the “Midsize Credit Card segment” by customer satisfaction in 2021. Whether consumers truly love the card is a more complicated question. Early in its life, the Apple Card was accused of gender bias in offering credit, though a thorough investigation by the New York State Department of Financial Services found no evidence of discrimination. Last month, Goldman revealed the bank’s credit card division was subject to a probe by the Consumer Financial Protection Bureau (CFPB), raising the specter of fallout. The CFPB is looking at how Goldman handles billing issues, refunds, credit reporting to bureaus, and advertising.

Notably, the Apple Card is by Goldman Sachs and not Marcus. While Goldman has managed to bring other collaborations like its work with General Motors under that banner, Apple preferred to use the financial institution’s more recognizable moniker.

This year has seen Goldman and Apple expand their partnership, though perhaps not with the depth the financial institution might have hoped. Goldman will be the loan issuer for Apple’s upcoming “buy now, pay later” (BNPL) service, but critically, the device-maker has internalized underwriting responsibility. As Apple grows more confident in provisioning financial services, it may find Goldman less useful.

Marquee

Released in 2014, Marquee builds on the foundations of SecDB, the platform that helped Goldman steer through the financial crisis. It represents one of the firm’s early attempts to externalize itself, taking some of its best technology and opening it up to clients. The product opens access to Goldman’s risk, data, and analytics capabilities and can be provisioned via API.

Marquee is also significant in that it serves as Goldman’s response to the advent of multi-dealer platforms like TradeWeb. Clients can execute trades via the service, turning what used to be a phone call into a few clicks. Though Marquee may be as easy to use as a service like TradeWeb, it does not open up customer trades to other dealers, meaning there is no competition over price. It represents a linear digitization of Goldman’s client relationship rather than a fundamental change in model.

Though Marquee is not the most revolutionary of platforms, it nevertheless demonstrates the evolution of Goldman’s enterprise tech efforts.

Transaction Banking

Transaction Banking, or “TxB,” is a more adventurous effort. Traditionally, the space has been dominated by JPMorgan, Citigroup, and Bank of America. All help enterprises manage cash, transmit money internationally, and mitigate risk. Such treasury services are lucrative, with transaction banking’s global revenue surpassing $1 trillion.

To compete with incumbents, Goldman has turned to tech. TxB is a self-serve tech platform that handles managing liquidity, payments, escrow, and other banking as a service needs. As with Marquee, it is API-enabled. Goldman has bolstered the platform by partnering with heavy-hitters like American Express, Fiserve, Visa, and Stripe. The bank’s collaboration with the last of those companies is particularly interesting. In 2020, Stripe rolled out its Treasury product with Goldman Sachs powering the storage and movement of funds.

Since its launch, TxB has expanded to the United Kingdom, with many more geographies on Goldman’s list. Division head Hari Moorthy expected the platform to reach 36 countries by mid-2023.

The Financial Cloud

Marco Argenti will take over as the sole Chief Information Officer in October this year. The former Amazon Web Services (AWS) VP has been at the firm since 2019.

One of Argenti’s primary initiatives is what Goldman refers to as “the Financial Cloud.” The project seems to be as much about organizational change as technological innovation. One source remarked that the project details were fuzzy but evoked something of Amazon’s corporate structure that seeks to turn teams into metaphorical APIs – able to call and be called upon quickly and flexibly.

More concretely, the early iterations of the Financial Cloud focus on analytics and data streaming, powered by AWS. Institutional clients can build on top of this information to create applications and analyses that serve their needs. Former CIO Marty Chavez was said to be the first leader who prioritized the developer as a client; the Financial Cloud continues that evolution.

Every Sunday, we unpack the trends, businesses, and leaders shaping the future. Join 63,000 others today.

Mixed fortunes

There are many ways to measure success. A company might judge an initiative on the number of customers it attracts, the revenue it generates, or the money it saves. It might consider softer measures, like consumer sentiment, strategic synergies, or cultural change. But for public companies, especially of Goldman Sachs’ size, there is ultimately one true scoreboard: the stock price.

By that measure, Goldman Sachs’ tech efforts have struggled to break through. On a price-to-book value basis, Goldman Sachs trails its rivals. Morgan Stanley’s P/B stands at 1.637, and JPMorgan’s is at 1.380. Goldman comes in at just 1.083. This isn’t an artificial low – the bank’s average for the past five years is 1.100.

Commentators have argued that Goldman’s spending on technology has hampered its valuation. Brennan Hawken, a research analyst at UBS, summarized the claim: "If they weren't making these investments, the stock would probably be higher.” CEO David Solomon has argued that the market gives Goldman “no credit” for what it has achieved with technology but that the “strategy is working” and will deliver compounding returns eventually.

Time will tell whether that is the case. In the meantime, we can look at other measures to judge Goldman’s performance. As we’ll see, the bank’s tech strategy has neither been as worthless as some outsiders might suggest nor as unblemished as the firm would have you believe.

Growth at a price

Here is a number that should impress you: Marcus has 14 million customers. That figure puts the product in elite company, surpassing U.S. neobanks like Chime (13 million) and Current (4 million). However, it is far from payment-focused products like Venmo (70 million) and Cash App (44 million). Interestingly, many of these customers have come via the Apple Card tie-in. Out of the 14 million Goldman amassed, the Apple partnership contributed “high single digit [millions],” according to one report.

Total consumer deposits surpass $110 billion, another sizable figure. If Goldman’s goal is to build a stable, inexpensive source of funding, it seems to have made an excellent start.

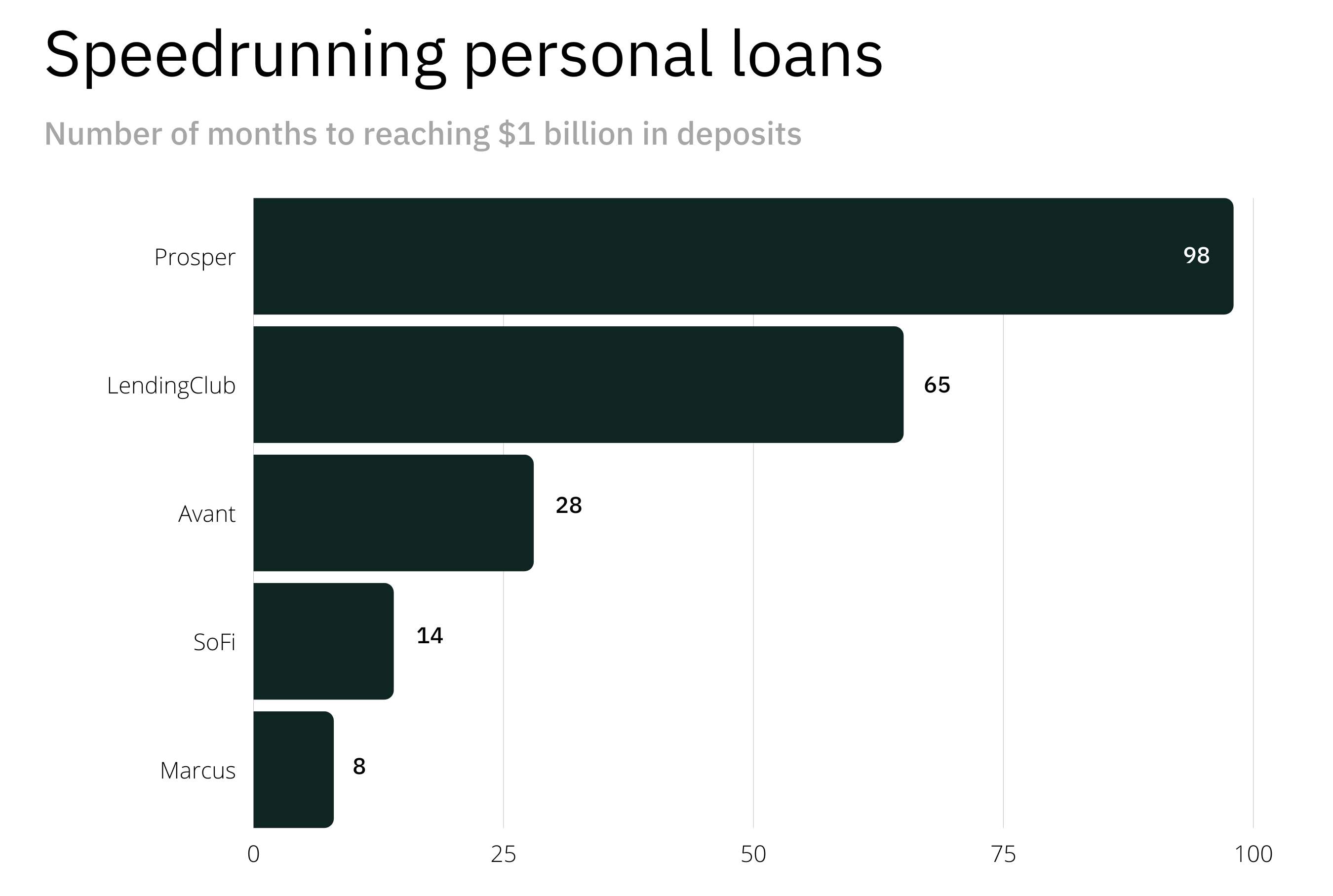

The pace of this growth is particularly impressive. Marcus is not quite six years old but has already become a mainstream product. This breakout trajectory was evident even in Marcus’ early days. It took the unit just eight months to issue $1 billion in total loans. By contrast, venture-backed players like LendingClub and Prosper needed more than five and eight years, respectively. By 2024, Goldman expects its consumer business to generate $4 billion in revenue.

To make such headway when steering a ship of Goldman’s size is no mean feat and speaks to the seriousness of the firm’s efforts. However, such success requires context. One source noted that Marcus had been seeded with a cool $1 billion. In the years since, the firm is believed to have spent over $5 billion on the effort, logging heavy losses. That figure doesn’t include the billions used to acquire GreenSky. Losses are not expected to slow, with a $1.2 billion deficit expected this year.

According to one source, part of that profligacy may come from the fact that Goldman doesn’t have obvious consumer distribution advantages. When signing up new customers, it has to use the same weapons as other companies: online ads, direct mail, and media spots. In a crowded category, winning a new user can prove costly. As discussed, it’s notable that most of Marcus’ customers have come via Apple – a channel it did not have to build.

Ultimately, Marcus has become a widely used product, but that has come at a steep, growing cost.

Disjointed consumer products

Despite Marcus’ traction, many are yet to be convinced by the effort. While Goldman’s aggressive spending on the unit is part of that suspicion, another element is the product suite’s incoherence. Jason Mikula, formerly a VP of Marcus and author of Fintech Business Weekly, remarked that “the business unit has gone a lot of different directions.”

Another source cited this as a critical error. Look at Goldman’s consumer efforts, and you can see their point. In six years, Marcus has fanned out into a confusing range of products that often seem geared toward different customer bases. The high-yield savings account appeals to affluent consumers, while personal loans target those with debt, for example. As for Marcus Invest – it may be a case of the less said, the better. Mikula described it as “very unimpressive.”

Perhaps because of these disparate identities, Goldman seems to have struggled to cross-sell its services. Though the firm doesn’t share precise figures, a source suggested such activity was uncommon. Greater focus may be needed to get the most out of Marcus.

Promise in platform

Goldman’s enterprise strategy feels more coherent. It leverages the bank’s existing client base and can be cross-sold by teams that service those companies.

Transaction banking seems to have been a particular success. When the platform first launched in mid-2020, Goldman set two five-year targets: to reach deposits of $50 billion and revenue of $1 billion. Eighteen months later, TxB hit $50 billion in deposits; in 2021, it delivered $225 million, up 50% from the year prior. At that rate, it should exceed $1 billion in revenue by its goal of 2025.

Parsing Marquee and Financial Cloud efforts is trickier. Goldman does not share revenue figures for Marquee, though it is part of the Global Markets division, which delivered $22.08 billion in 2021 net revenue. Much of that may still occur through traditional channels, though having a sophisticated online platform is a boon. Though the firm’s cloud initiative seems a priority, it is too hazy to judge.

By and large, Goldman seems to have found a way to turn itself into a platform much more effectively when it comes to serving enterprises.

Cultural change

One-third Goldman Sachs. One-third consumer finance. One-third Silicon Valley.

According to a source, that was the recipe Goldman Sachs hoped to emulate with Marcus. To do so, the firm would need to change its culture and recalibrate its talent pool fundamentally. With the benefit of hindsight, it seems as if Goldman has succeeded and failed.

On the one hand, Goldman made some smart moves when building out Marcus’ tech team. Rather than shunting the division into a subsidiary office, it kept them in-house so that lines of communication could remain fluid. Over the years, the bank has succeeded in recruiting able talent, with a different source noting that the last two years had seen a record number of employees join from other tech companies.

Beyond Marcus, other positive shifts have occurred. Traditionally, Goldman divided itself between front and back offices. The latter was referred to as “the Federation.” Historically, engineers operated from the Federations hinterlands, but recent years have seen them pushed into front office teams, allowing for greater connectivity. A source described it as an excellent cultural move.

While Goldman seems to be a better place for engineers than in the past, it nevertheless has to pay above market rates. Those that join don’t get equity in a fast-growing startup; to compensate, they have higher salaries. Not only does this increase Marcus’ operational costs, it changes alignment. Though recruits receive stock-based compensation, they may not feel like owners in the same way they would at a startup. One source added that though Goldman can hire able tech talent, it cannot compete for elite practitioners. Whereas once enterprising young professionals dreamt of getting tapped to attend 200 West Street, modern counterparts covet roles at Google or Stripe.

To compete with leading fintechs, Goldman will need to recruit and motivate equivalently strong talent.

What next?

In the context of Goldman’s 153-year history, its tech initiatives are just a blip. While no business can afford to rest on its laurels, the firm can take the long view. Underperforming elements can be trimmed, promising products can be bolstered, and culture can continue to adapt to new challenges. David Solomon may not be right that the market misjudges Goldman’s technical accomplishments, but he can still guide the company toward compounding returns.

Streamline

This year, Goldman is expected to add another product to the Marcus suite: checking accounts. Slated for release in 2021, the offering is in beta with Goldman staff members and will finally launch later this year.

It’s easy to understand Goldman’s strategy here. Checking accounts are often loss leaders, but they are a customer’s primary financial relationship. If Goldman wants to own consumer banking, having a high-contact hub like this may be necessary.

It also feels like a repeat of past mistakes. Marcus’ problem is not that it has too few products but too many. As we’ve discussed, these often don’t connect as coherently as Goldman might wish and run at a considerable cost.

If Goldman is to turn Marcus into an unqualified success, it should pare back on relatively undifferentiated products with high customer acquisition costs. An easy example is Marcus Invest. It is an unremarkable product that competes against fuller featured offerings with long headstarts. Persuading customers to choose the service over Betterment and Wealthsimple will likely require sustained engineering and marketing costs with no promise of victory.

Marcus’ checking account endeavor feels like a similar proposition. The company is going after a well-banked consumer base – people that likely use JPMorgan Chase or a similar service. What can Marcus Checking offer that will break through the flurry of direct mail promotions? What killer feature will make this kind of customer go through the pain of switching banks?

Marcus’ loan products should not be exempt from downsizing. This may sound like sacrilege. On some level, the product is clearly working. It wins awards and has managed to grow deposits quickly. But it still does not feel strategically coherent. The customer profile sits at odds with Goldman’s other consumer efforts, and it looks like a continued financial drag. Goldman can find more impactful ways to deploy its capital.

Double-down

Rather than entering a CAC war with banks in established categories, Goldman should consider taking a page out of the Transaction Banking book. Part of the reason that initiative is so interesting – and seems to be working so well – is that it leverages Goldman’s natural advantages. This is a business with connections to every meaningful fund and company on earth, with an elite brand that makes it an attractive partner. It has global banking licenses, a massive balance sheet, and modern tech infrastructure.

In the coming years, the firm should look to lean into these strengths rather than attempting to build new ones from scratch. That should involve investing in the expansion of TxB and finding other opportunities to externalize its capabilities. The Financial Cloud initiative looks set to attempt something similar and is the kind of bet the firm should be making.

This doesn’t mean that Goldman needs to forgo amassing more consumer deposits – only that it may wish to do so via a different motion. The Apple Card provides a perfect case study. Instead of winning over customers itself, Goldman leveraged its partner's distribution power. While a source remarked that the firm had built the infrastructure for the Apple Card in a fairly custom way, it’s easy to imagine how it could turn this into a broader platform. In the future, Goldman could provide banking services for companies like Instacart, Airbnb, Glossier, Epic Games, and beyond.

At times, Goldman has acted as if it believes the prize to be won via technology is to emulate Chase or Discover. It must realize that it is far better positioned to become the embedded banking partner to the world’s innovators.

Find new champions

Though Goldman has made progress in incorporating technology into its culture, one source noted that it still has a way to go. They mentioned that the people celebrated at the firm are still primarily on the financial side. There are star bankers and traders but few star engineers or product managers. The names mentioned in reverent tones by employees are inevitably those that work in the securities division, not those in Argenti’s orbit.

This will need to change if Goldman is serious about becoming a tech company. Having a technologist like Argenti in senior leadership is a good start. Over the following years, the firm should look to add more engineering and product talent to its upper ranks and find ways to celebrate (and generously bonus) those that excel in these functions. The goal should be to reach a stage in which consequential business decisions are consistently made by, or with, tech-native managers.

“We are a technology firm,” former CEO Lloyd Blankfein said in 2017, “We are a platform.”

Today, that seems only partially true. While Goldman Sachs has built a considerable consumer practice and some exciting enterprise solutions, it does not feel like a tech company. It does not act like one. Engineering still seems to be treated like a cost center, and though its status has risen, it still trails traditional financial functions.

And yet, it is easy to be too critical. To want more from what may be the world’s most prestigious bank. Goldman has come a long way. It has launched new products, acquired millions of customers, and accumulated billions in deposits. It has worked with tech’s most innovative organizations, pushing them and allowing itself to be pushed; it has opened itself to change. That we can have such conversations about its failings is a triumph in and of itself. Only those that dare to reinvent themselves can hope to live forever.

The Generalist’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice. You should always do your own research and consult advisors on these subjects. Our work may feature entities in which Generalist Capital, LLC or the author has invested.