Ho Nam on VC’s Power Law

Lessons from Arthur Rock, Steve Jobs, Don Lucas, Paul Graham and beyond.

🌟 Hey there! This is a subscriber-only edition of our premium newsletter designed to make you a better investor and technologist. Members get access to the strategies, tactics, and wisdom of exceptional investors and founders.

Friends,

We’re back with our latest edition of “Letters to a Young Investor,” the series designed to give readers like you an intimate look at the strategies, insights, and wisdom of the world’s best investors. We do that via a back-and-forth correspondence that we publish in full – giving you a chance to peek into the inbox of legendary venture capitalists.

Below, you’ll find my second letter with Altos co-founder and managing director Ho Nam. For those who are just joining us, Ho is, in my opinion, one of the great investors of the past couple of decades and a true student of the asset class.

Because of his respect for the practice of venture capital, I was especially excited to talk to him about today’s topic: learning from the greats. Who were Ho’s mentors? Which investors does he most admire and why? What lessons from venture’s past should be better remembered by today’s managers?

Join our premium newsletter, Generalist+, to read the full correspondence and unlock a library of investing wisdom.

Lessons from Ho

Prepare for one true winner. Even skilled investors often have just one or two outlier bets over the course of their career. Because of venture’s power law, their returns may dwarf the dividends of all other investments combined. Your mission is to find these legendary businesses, engage with them deeply, and partner for decades.

Focus on the company. Venture capital is full of short-term incentives. Instead of focusing on raising new vintages or building out Altos as a money management firm, Ho and his partners devote themselves to their portfolio companies. Though firm building is important, if you find great companies and work with them closely, you will have plenty of available options.

Pick the right role models. Ho chose his mentors carefully. Though there have certainly been louder and flashier investors over the past four decades, Ho learned the most from Arthur Rock, Don Lucas, and Arnold Silverman. All were understated and focused on the craft of investing. Find the people you consider true practitioners, and study their work.

Watch and learn. Learning from the greats can be done from a distance and may not include a memorable anecdote or pithy saying. Ho’s biggest lessons came from observing the habits of practitioners like Rock and Lucas, not via a structured mentorship or dramatic episode. It’s by studying the everyday inputs of the greats that you may gain the most wisdom.

Mario’s letter

Subject: Learning from the greats

From: Mario Gabriele

To: Ho Nam

Date: Friday, April 12 2024 at 1:59 PM EDT

Ho,

After moving out of New York City (at least for a little bit), I’m writing to you from a small house on Long Island. It’s been really lovely to have a bit more space and quiet away from the city’s intermittently inspiring and exhausting buzz. I have been enjoying some meandering forest walks with my dog, reading the exceptional novel Demon Copperhead, watching The Three Body Problem adaptation (I suspect you’d really enjoy the books if you haven’t gotten to them yet), and trying to learn more about the world of robotics. I’d love to hear what’s animating your springtime, both in and out of the office.

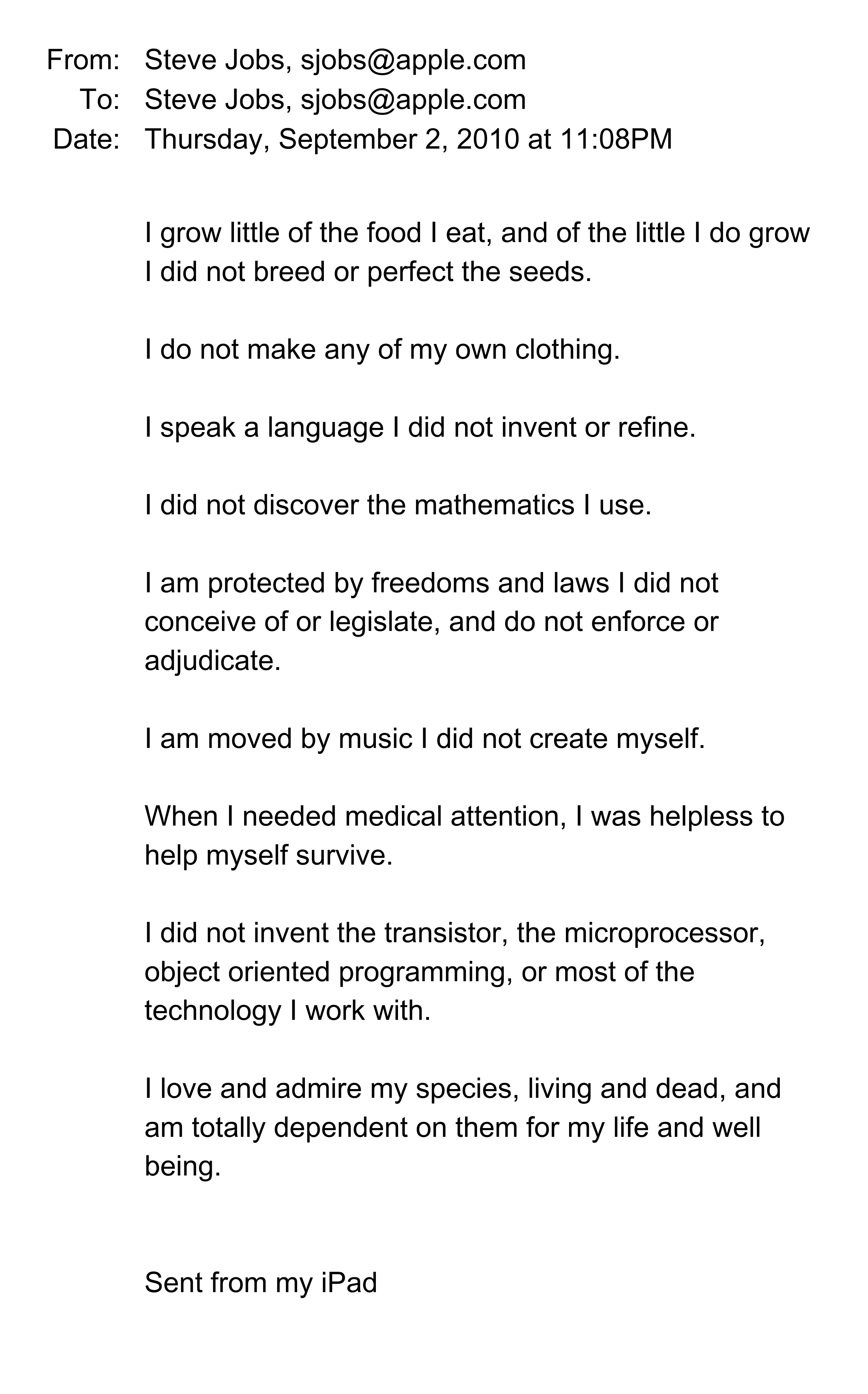

I recently came across a message Steve Jobs sent to himself roughly a year before his death. I imagine you know it well, as will many readers. In it, Jobs reflects on an aspect of the human condition. Namely, that all of us rely on each other and the innovations of our ancestors. It’s his version of Isaac Newton’s phrase, “If I have seen further, it is by standing on the shoulders of giants.”

The Jobs memo reminded me of our conversation for a couple of reasons. For one thing, its application to the craft of investing. Every great investor refines their abilities through mentorship, competition, and conversation. Buffett would not be Buffett without Munger, Graham, and even, perhaps, the One Thousand Ways to Make $1000 book he borrowed from the library as a seven year old. No one succeeds alone.

Secondly, Jobs’ email reminds me of legendary venture capitalist, Arthur Rock. I first learned about Rock through you and eventually wrote a piece about his remarkable career. As you know well, Rock was an early backer of Apple, writing a $57,400 check in 1997. Jobs later referred to Rock as something of a father figure.

I share this background because it forms the basis for an aspect of your craft I’d love to explore together. As you look back on your 34 years of investing, from starting out at Trinity Ventures to building Altos, who are the people you’ve learned the most from? What have they taught you? These might be people you worked with, of course – your old bosses and current partners, for example – but might also be figures you studied from afar. From our last exchange, I know that Buffett is one of them, of course.

Above all, I’d love to understand the stories behind the pieces of advice you’ve received and how they’ve impacted the way you analyze investments and make decisions. What company might you have missed without the right guidance? What mistake could you have avoided if you’d listened to a mentor’s advice?

Though I am just beginning my investing career, there are a lot of pieces of advice I’ve gathered that I find helpful when evaluating a startup. A few examples:

Anomalous outcomes come from anomalous people. Many of us are raised with a very conventional idea of what a “successful” person looks like. They are polite, well-spoken, intelligent – graduates of good universities and holders of prestigious jobs. While elite founders may have this kind of background, many do not. In studying Hummingbird Ventures, I have come to appreciate exceptional entrepreneurs’ lesser discussed characteristics; for example, enduring childhood trauma or displaying neurodivergence. Keeping those ideas in mind reminds me to look for truly anomalous individuals.

Leaning into your winners. Virtually every great vintage seems to have been built on this lesson. You mentioned in your last letter how Altos aggressively tripled down on Roblox, despite countervailing incentives. Another example is Blackbird Ventures, an extremely impressive firm focused on Australia and New Zealand. Their first vintage (2013) has a net TVPI of 32.64x. When I asked founder Niki Scevak how he’d managed that, he told me that at least half of those returns came from aggressively building onto their position in Canva.

Great companies often start out looking like “toys.” That Clay Christensen theory, popularized by Chris Dixon’s excellent essay, remains relevant. Megahits like Meta, Airbnb, and Roblox all started life as projects that a less open minded person would have dismissed as frivolous. It takes a certain optimism and farsightedness to look at a “toy” and see what it could become.

Look for animals. Paul Graham has a litmus test for hiring: could the candidate in question be described as an “animal” with a straight face? It’s a simple heuristic but one I find useful in evaluating founders. Animals can come in all shapes and sizes; they can be quiet or loud. But you know when you are speaking to one.

Beware of red flags. In the wake of the FTX disaster, Bill Gurley shared a list of “red flags” investors should keep in mind. It includes the lack of a legitimate board and having an odd corporate HQ, among others. Though I think it’s in a venture investor’s best interest to be optimistic, they should never be thoughtless.

Never outsource your decision-making. The nature of venture means that even the world’s very best investors will be wrong most of the time. Although it can be tempting to join a round simply because John Doerr, Vinod Khosla, or Keith Rabois are backing it, that is a fool’s errand. You have to do your own rigorous underwriting and choose for yourself. Otherwise you end up building someone else’s portfolio. I have mostly learned this by studying investors that make truly independent decisions (like you and Altos).

The importance of focus. It’s tempting for a venture firm to try to do too much. In studying Kleiner Perkins, I learned how running multiple practices (early stage, growth, overseas) can split a team’s focus, create factions, and dilute performance. While there are funds that manage to run multiple practices, there is power in knowing the game you are playing and focusing on it relentlessly.

Asking whether a company can be one of the most important in the world. I actually can’t remember where I first heard this – I think it’s a Founders Fund framework? Hopefully, a reader can tell me :) The primary idea is to ask yourself whether the startup you’re considering investing in can become one of the most important companies on earth. I find it a helpful way to test whether I’m taking a big enough swing and respecting venture’s Power Law.

Playing the long game. There are lots of ways to earn short-term social capital in venture investing. You can invest in a lot of companies quickly (demonstrating activity), chase logos (suggesting taste), or squeeze in to invest alongside brand name funds (proving access). Some of these approaches might work for a time. But in the long run, no amount of manufactured cache will help you. The only things that matter are the companies you helped and the capital you returned to investors.

I’d be curious if these tidbits resonate, and whether there are pieces of advice that you keep returning to over the years.

Underneath all of my questions is a final strand: what advice would you give to today’s investors? What does the current generation appreciate too little or praise too much? How can younger venture capitalists improve their chances of having the kind of remarkable career you’ve managed to build?

I’d love to hear any of your thoughts, from the tactical to the theoretical.

Thank you for sharing your wisdom!

Best,

Mario

Ho’s response

Subject: Learning from the greats

From: Ho Nam

To: Mario Gabriele

Date: Monday, April 22 2024 at 6:55 PM PDT

Mario,

Those are such great lessons, and I also owe so much to generous mentors over time. I think there is also a lot to be learned from what NOT to do and there are many people who taught me such great lessons. Examples of what not to do include not facing reality and exhibiting self-serving behavior, which may benefit you in the short term but cause harm in the long term by eroding trust. It’s a subset of behavior that I refer to as people digging their own graves.

One of the most important lessons I’ve learned in my career overlaps with 3-4 of the ones you shared. It’s one that Charlie Munger has shared many times over the decades and is very much related to the power law of returns in venture capital. Charlie said that no one is so smart or so lucky to have more than a handful of great investments in a lifetime. I’d add that one of our companies does not have to be one of the greatest companies in history. All we need to know is that if we are fortunate enough to make many investments over decades, only a few (likely only one or two) will make all the difference. So, we are always looking for potential outliers within our portfolio. We look to deepen our understanding and relationship with a handful of companies, which leads to multi-decade partnerships.

If we, as a team, were able to do this only a few times in our lifetime, we thought we’d have a chance to become legendary VCs. We did not care about building our money management business. What we cared about was the legacy of our companies. If some of our companies can be great, then the track record would give us many degrees of freedom – to grow the firm or remain small, manage our own family office, etc. Decades ago, we did not know where we would end up, but we knew that if we did not take care of the primary goal (of building great companies), the secondary goal of building Altos would fail.

There is a paradox. For fund manager “entrepreneurs” who take the risk of leaving good jobs to start and build their own VC firms, the most obvious marker of success is raising new funds and growing AUM. But in achieving such goals, they may sow the seeds of their own destruction.