Sardine: Fintech’s Great Detective

The rapidly scaling startup is more than just a fearsome fraud prevention platform for fintech and crypto. It’s laying the foundation to become a payments giant.

Brought to you by Sardine

If you’re a fintech or crypto company, you should be using Sardine. It is that simple.

The fraud prevention and payments provider protects your customers from malicious scammers while improving your conversion rates. Companies like FTX, Brex, AtoB, MoonPay, Autograph, and others use Sardine to stop fraud and increase revenue.

To get started, book a demo here. By doing so, you stand to cut fraud by 300% and unlock $500,000 in operational savings.

Actionable insights

If you only have a few minutes to spare, here's what investors, operators, and founders should know about Sardine.

Beware the butcher. A new kind of fraud is taking hold: “pig butchering.” The gruesomely monikered scam involves manipulating someone into buying cryptocurrency, then transferring it to an external account to be “managed.” When it comes time to realize profits, the crypto is gone. Not only is this type of fraud brutal, it’s challenging to detect.

The Sherlock of scams. Sardine has built a defense against such bad actors. Using behavioral and device data, the startup can sniff out scammers. Among other data sources, Sardine observes how users scroll, click, and type to assess their risk.

An ideal team. Soups Ranjan built fraud systems at Coinbase and Revolut. The Sardine CEO deeply understands how financial crimes are perpetrated and what is needed to stop them. He’s joined by Aditya Goel and Zahid Shaikh – fintech obsessives that have worked at Revolut, PayPal, and JP Morgan Chase.

Powering payments. From the beginning, Sardine’s co-founders sought to build more than a fraud prevention platform. Instead, they wanted to use this service to provide a game-changing payments processor. Today, Sardine handles payments for crypto companies and neobanks, using their fraud detection suite to improve conversion rates.

True network effects. The company wants to create a fraud directory that compiles data from the industry and which companies continue to update. For example, if an email address is associated with fraud on Chase, a neobank like Revolut will see the information has been flagged. This is a product with obvious network effects.

This piece was written as part of The Generalist's partner program. You can read about the ethical guidelines I adhere to in the link above. I always note partnerships transparently, only share my genuine opinion, and commit to working with organizations I consider exceptional. Sardine is one of them.

Dejan Davidovich knew what was happening. He just didn’t know how to stop it.

In 2019, Davidovich’s life descended into a nightmare. The COO of European cryptocurrency exchange Kriptomat had been summoned to court, questioned at the Estonian airport, and inundated with customers threatening legal action. Nearly all stemmed from the same source: a ruthless scam.

It worked something like this:

Imagine you’re browsing Facebook one day when you come across what looks to be a news article. (It is likely an advertisement.) In it, a novice investor details the life-changing money they’ve made investing in cryptocurrency. They attribute their profits to the help of a wealth management firm that specializes in the sector, linked in the piece.

Intrigued, you click through to the firm’s website. You might be especially predisposed to this if you’re struggling financially; a quick windfall might make all the difference in your life. The wealth management firm asks you for a few simple pieces of information: your name, email address, and phone number.

A few minutes after you register, you get a call. A representative from the wealth management firm notes they received your application and would be happy to kickstart your crypto investing journey. To get started, would you mind downloading remote access software? TeamViewer or AnyDesk is fine – the important part is that the representative can take control of your screen, helping you through the pesky onboarding process cryptocurrency exchanges demand.

You comply. The representative seems knowledgeable and helpful, and navigating a new platform is intimidating. It would be so easy to make a mistake.

With remote access set up, you watch as the representative whips through the sign-up process on an exchange called Kriptomat, occasionally pausing to explain something or ask for information. You share your address, bank details, and identifying information. If all goes smoothly, this takes a few minutes, after which the fun part begins. Now that you’re registered, you can pick a cryptocurrency to invest in. Perhaps bitcoin or ether? The representative tells you those are good bets, but it’s important to start small. You can always add more over time.

You decide to invest €300 in bitcoin. Not a lot, but not a little.

A few minutes later and the bitcoin hits your account. The representative congratulates you: you’re officially a cryptocurrency investor! The only thing left is to transfer the bitcoin to the wealth manager’s wallet address. That way, they can work on growing the value of your holdings. Don’t worry; you can see your crypto on the wealth manager’s handy online platform.

One might think: this is where it ends. The crypto has been sent into the ether; the scam is complete. Often, that’s not the case. Instead, it extends for months, growing increasingly brutal.

When you check your wealth management account a week later, you see that your funds have grown significantly. The firm is doing an exceptional job, and everything you read about the money to be made is proving to be true. Impressed by your early returns, you decide to invest more. Your representative is happy to help, guiding you through the purchase flow and taking over to handle the annoying process of sending bitcoin from one wallet to another.

In the months that follow, you keep investing. Why wouldn’t you when the returns are this good? Hundreds of euros turn into thousands and tens of thousands. Soon, you’ve pushed your life savings into crypto in the confidence that whatever you put in, you’ll get back tenfold. After all, you’ve seen it happen.

After a time, you decide to take out some of your profits. You’ve done so well and could use a little liquidity. Only then does the hammer drop.

When you email your representative, you get no response. When you call, the line is disconnected. When you try to withdraw from the wealth management website, nothing happens. When you try again, you’ve been locked out.

Everything you invested has gone. Everything you earned was a lie. You have been “pig butchered,” as the practice has come to be known. Fattened up and slaughtered.

For many, this is a crippling moment. It is a confusing one, too. Who is to blame? Bewildered by what has transpired, many misdirect their anger at the exchange rather than the fabricated wealth management firm. Kriptomat has stolen their money, they decide, not the kind representative that had been so helpful. It probably doesn’t help that there is no longer a wealth advisor to aim allegations at, while Kriptomat’s customer service tries to help. The latter absorbs the pain caused by the former.

This is true in myriad ways. Kriptomat incurred costs beyond customer ire and significant aggravations to the lives of executives like Davidovich. Partners began questioning Kriptomat’s integrity, regulators considered fines, and banks blocked connections to the exchange. “It’s not just the customers that get affected,” Davidovich noted, “The business gets affected, too.” A once-promising startup suddenly seemed in jeopardy.

What was Davidovich to do?

From speaking with customers, he discovered how the scam had been perpetrated, but he couldn’t figure out how to defend against it. After all, on Kriptomat’s end, those being guided by the fraudsters looked like any other customer. Their information was up-to-date and accurate. They passed KYC checks. How could you tell something was wrong? How can you detect an invisible crime?

Founded in 2020, Sardine has made its name by solving fiendish cases like this one. The fraud prevention and payments platform saves companies from serious jeopardy and allows them to grow without fear. The resulting startup is a mix between Sherlock Holmes and Stripe – a growing fintech power player with near-miraculous observational skills.

Today’s piece will explain how Sardine solved the Case of Kriptomat. We’ll also explore how the company’s groundbreaking fraud capabilities position it to take a big bite out of the payments market. Here’s what to expect:

Origins. Without knowing it, Soups Ranjan was preparing to build Sardine for the entirety of his professional life. The startup’s CEO has a deep background in security, with robust experience building fraud prevention for crypto and fintech.

Product. Sardine is an elegant, thoughtful business. The different elements of its product offering work together to create a neat flywheel spanning fraud, payments, and broader risk insights.

Culture. Great companies often manage to recruit people that are talented enough to run businesses of their own. Sardine has a roster that has led organizations across the fintech landscape.

Future. Sardine is already a large, effective business. But if it wants to reach super-scale, it must ensure it navigates the competitive landscape, finds the right positioning, and cultivates powerful network effects.

Every Sunday, we unpack the business world’s most important innovations and the stories behind them. Join 63,000 others today.

Origins: Dream team

Exceptional companies often emerge when a promising idea intersects with a singularly well-positioned entrepreneur. Sardine is a clear example of this phenomenon. Soups Ranjan spent years building fraud prevention software at fintech and crypto companies like Revolut and Coinbase. That experience allowed him to see the gaps that Sardine has been able to fill.

The game is afoot

Ranjan decided to take a leap. After receiving a Ph.D. in Electrical and Computer Engineering from Rice University, he had built an impressive career in cybersecurity. Over a decade, Ranjan had constructed systems designed to sniff out bad network traffic and click-fraud at companies like Google and Yelp. He had even started a company of his own, focused on expense tracking.

In 2015, Ranjan decided to make a change, joining a growing startup called Coinbase. At the time of his arrival, the price of bitcoin flitted beneath $300, and the cryptocurrency exchange had fewer than fifteen engineers. Though he had an extensive history in fraud and cybersecurity as it related to e-commerce and social media, Ranjan was not only new to crypto but fintech, too. “I didn’t know anything about payment fraud until I started at Coinbase,” he admitted.

Ranjan’s role as Coinbase’s Director of Data Science & Risk required him to get up to speed quickly, especially as interest in the sector ramped up through 2016 and 2017. To extend his expertise and meet other professionals, Ranjan founded a network and event series dubbed the “Risk Salon.” Every month, peers met for roundtable discussions about the state of the industry, new vulnerabilities, and prevention methods. The organization grew to more than 500 members with more than fifty hosted events. “It became really, really big,” Ranjan said.

It proved a compounding advantage. As we’ll discuss, not only did Risk Salon help Ranjan thrive at Coinbase, it allowed the future CEO to develop a world-class network that he could leverage for partnerships and subsequent recruitment.

Ranjan quickly learned that the fraud Coinbase faced was fundamentally different than the types he’d encountered previously, especially in the e-commerce world. “E-commerce is transaction-based,” Ranjan explained, “The concept of a user doesn’t really matter. What you’re focused on is the shopping cart.” When making purchases online, fraud typically involved an incorrect shipping address or fabricated card number – these were the places scammers made their mark.

Solutions had emerged to tackle this problem, but they were of little use to Ranjan. “We couldn’t rely on them at Coinbase,” he said, “the fraud was totally different.” It had nothing to do with shipping addresses and rarely involved card details. What the Director of Risk realized was that the majority of fraud came from customers that had been verified, passing KYC checks and other approvals.

In many respects, this must have been a dizzying revelation; the fintech equivalent of horror movies’ “the call is coming from inside the house” trope. The threat is different, closer than imagined.

Ranjan realized that to combat it effectively, Coinbase needed a new toolset. He settled on the right vectors for observation by deduction: “You’re left with just two dimensions: behavioral data and user device data.” If Ranjan couldn’t detect fraud by looking at a customer’s information, he would do so by observing how they and their device acted.

What device were they using? How quickly did they navigate to the correct tab? Did they copy-paste their own name into the signup fields?

Each of these was a clue, a tell, an indication of who was on the other side of the screen. Just as Sherlock Holmes could deduce a character’s life story from a seemingly disconnected cloud of observations – finding meaning in a limp, a stain, a scent – Ranjan knew that software could make judgments from scrutinizing device and behavioral data.

Not all fraud fell into the “fake investment advisor” category. Another common crypto scam took advantage of the increasing speed of payments. One product manager in the space explained that some ill-intentioned users would initiate the account funding process, buy crypto, send it off the platform, and then cancel the funding before it had settled.

Over more than three years at Coinbase, Ranjan devised solutions to protect against some of these attacks, learning just how difficult it was to build robust security of this kind. He would soon learn that crypto was not the only sector struggling with such issues. Across the fintech world, customer funds were under attack.

The Fraud Commandments

In early 2019, Ranjan joined neobank Revolut as Head of Fincrime Risk. His new employer faced similar challenges as Coinbase. Like the crypto exchange, Revolut had to identify scammers from a customer base that often had all of the correct identity data. As he had already learned, users that passed KYC checks might still commit fraud.

Tasked with scaling Revolut’s business in the US and a burgeoning crypto unit, Ranjan developed an even keener sense of how fraud impacted an organization. Even impressive, fast-growing players like Revolut could find progress slowed or stymied by the specter of fraud. Something as simple as transferring money from a bank account to a Revolut debit card carried considerable friction, with roughly 50% of transactions failing. “It was awful,” Ranjan said of this struggle.

While frustrating, the reason this occurred was perfectly logical. “It’s all a question of incentives,” Ranjan said. In this case, the originating bank – usually a big player like JPMorgan Chase or Bank of America – didn’t have a sufficiently accurate way of assessing Revolut’s risk as a counterparty. “They see neobanks as a very easy way to steal money,” Ranjan explained. There’s good reason for this much of the time. Neobanks and robo-advisors often have a higher average fraud rate, around 0.30%. Though that may sound low, it’s three times the rate of traditional debit cards. Given the thin margins banks rely on, even a few basis points can make a real difference.

Because of this, banks often don’t want to take on the extra risk. They decline newcomers en masse, using a machete when a scalpel is preferable. Attempting to grow a new business line when half of your customer base is thwarted at the first hurdle proved difficult.

For Ranjan, it also cemented a few non-obvious truths about the world of fintech fraud. Taken together, we might call these the Fraud Commandments of online payments:

Identity verification ≠ fraud prevention. Knowing who your users are is insufficient. The majority of fraud comes from customers that have been fully verified.

Prevention must move at the speed of transactions. Money movement is almost instant, but traditional fraud checks can take days. To combat bad actors, you must move as fast as the transactions themselves.

Fraud doesn’t matter…until it’s the only thing that matters. Early on, fraud may not be a big problem for your business. But whenever it hits, it is existential, affecting growth, revenue, and customer experience. It also threatens long-term reputational damage.

Revolut clarified these truths for Ranjan. It also introduced him to his co-founders. Aditya Goel worked as Head of Product and Operations for the US division, while Zahid Shaikh was the product owner of crypto. Both of them had considerable experience in the financial sector. Goel had served as a VP of Product at Deutsche Börse Group, owner of the Frankfurt Stock Exchange. While there, Goel managed the creation of open APIs and other tech-forward products. Meanwhile, Shaikh had worked at Chase, PayPal, and Uber, bringing an understanding of payments and fraud that spanned traditional finance and tech.

Together, the three of them led the construction of Revolut’s internal protections, allowing the neobank to grow in the US and beyond. “We built a lot of infrastructure in-house,” Goel said, “Primarily because what we needed didn’t exist.”

Ranjan describes his journey to starting Sardine as a “slow burn”; it is at this point that the idea ignited. Recognizing the significance of what they had built, the absence of solutions, and the strength of their team, the trio set out to create something of their own. In April 2020, Sardine was born.

An elegant machine

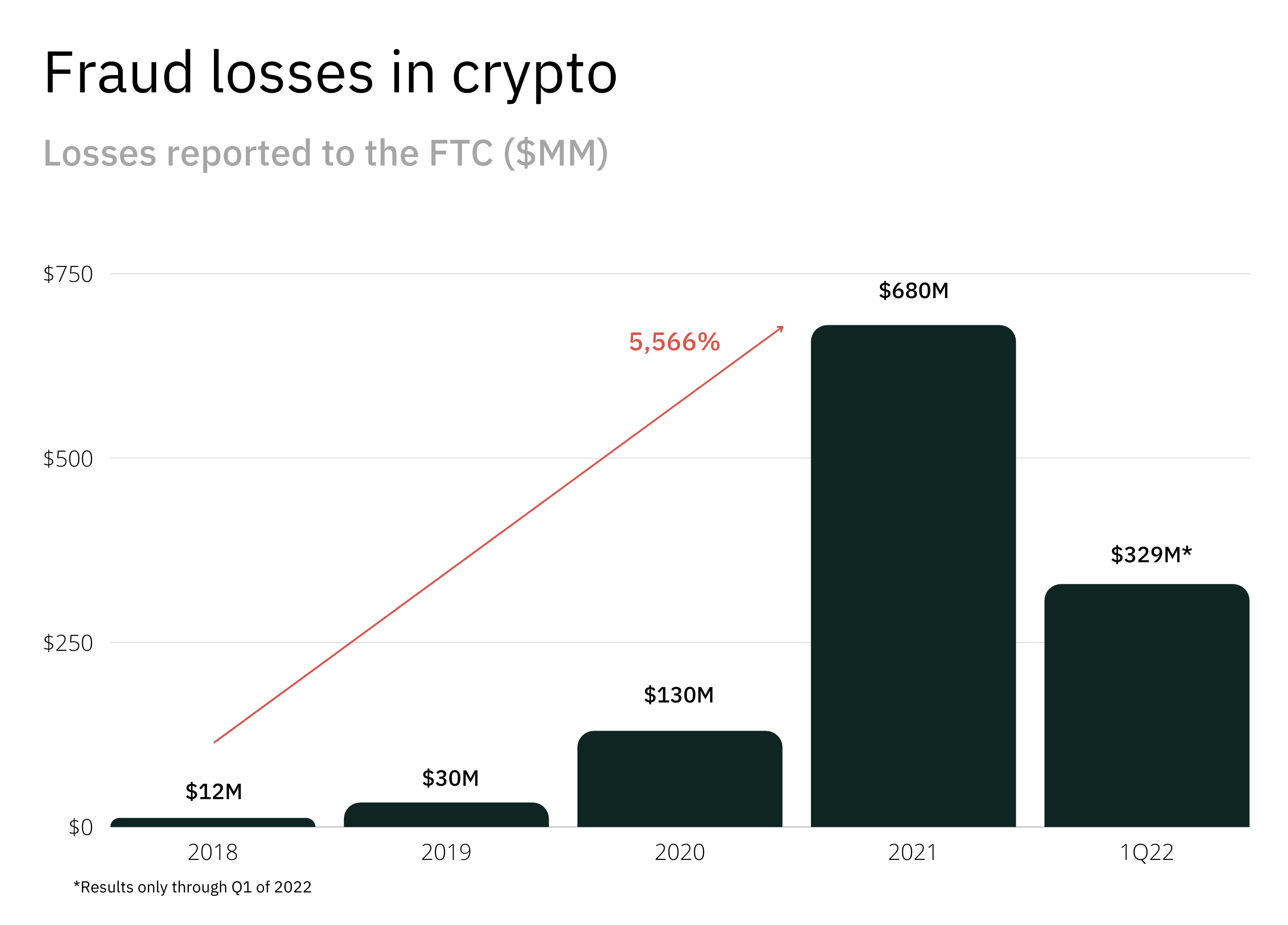

Though Sardine’s founders knew the scale of the opportunity they were addressing, it’s worth outlining the magnitude and growth of online fraud. A recent research report estimates that total online payment losses between 2023 and 2027 may reach $343 billion. Another source states that card fraud alone – some of which occurs online – may amount to approximately $50 billion annually by 2030.

Crypto adds a new dimension to these figures. In 2021, crypto crime totaled $14 billion, up 80% from the year prior. Another report from the Federal Reserve noted that 46,000 consumers had lost more than $680 million in combined losses in 2021, an increase of nearly 56x from 2018. Strikingly, this meant that approximately a quarter of all lost funds occurred via crypto, more than any other payment method. If money continues pouring into the sector over the next decade, future losses may dwarf such figures unless better protections are adopted.

Ranjan, Goel, and Shaikh were intimately acquainted with the problem. In Sardine, they set about designing an elegant solution.

At first glance, Sardine might have looked like a straightforward fraud product in its early days. Angela Strange, a GP at Andreessen Horowitz and eventual investor in Sardine, passed on the seed round for those reasons. “It looked like they were building a point solution in a sea of other KYC products, which might be the most crowded infrastructure space on the planet,” Strange said, “That was my screw up.”

While Sardine might have appeared to be yet another KYC provider, there was much more sophistication under the hood. For one thing, Sardine wasn’t interested in identity information alone, but in how it could be combined with the kind of behavioral screening Ranjan had built at Coinbase and Revolut. By bringing these pieces together, Sardine offered something far more potent than KYC verification.

It also had clear, bold ambition. Sardine’s founders didn’t want just to build a big company; they wanted to construct a generational one. To do so, they knew they would need to go beyond fraud. “We always knew we wanted to build a payments product,” Aditya Goel said, “but we wanted to solve for fraud first.” It was a progression that made sense. As their time at Revolut had demonstrated, imperfect risk assessments directly impacted transaction volume. If Sardine could better detect and prevent fraud, it could also earn the opportunity to handle payments. “Fraud and payments are two sides of the same coin,” Goel said.

Though playing in the payments world meant competing against much larger rivals like Stripe, Adyen, and FIS, it raised the company’s ceiling. “The outcomes for fraud companies tend to be around $3 billion,” Simon Taylor, Sardine’s Head of Content, remarked, “when you get into payments you can get to $10 billion or more.”

In the two years since Sardine’s seed round, the intelligence of the company’s approach has come into clearer focus, attracting considerable capital. After recognizing the savvy of Ranjan’s master plan, Strange moved aggressively to lead a $19.5 million Series A earlier this year. “It’s a very clever chess game they're playing,” Strange said.

Not long after, Sardine announced a $51.5 million Series B, led by a16z once again. Industry titans like Visa, Experian, ING Ventures, Cross River Bank, and Alloy Labs contributed; FIS had invested just before the Series B. Activant Capital also joined, with General Partner Andrew Steele seeing considerable potential in Sardine’s approach. “This is a real platform play,” Steele said, “they have the ability to totally unlock payments.”

As we’ll see, the product Sardine has built to attack this opportunity is powerful and differentiated.

Product: A fintech flywheel

The keen reader may already understand how Sardine solved the Kriptomat conundrum. How do you stop “pig butchering” without crushing growth? The clues are all there.

Dejan Davidovich searched for a solution to the fake advisor fraud endangering his platform’s 500,000 users – to no avail. “All of these providers were saying no, we can’t help with this kind of fraud,” he said. “But we couldn’t take no for an answer.” As a kind of Hail Mary, Davidovich posted on LinkedIn, outlining his problem and soliciting solutions. Luckily, Soups Ranjan saw the message. He responded to Davidovich, offering to show the COO what Sardine could do. He was confident his company could solve Kriptomat’s dilemma.

Thankfully for all involved, Ranjan was right. Compared to 2019, Kriptomat’s fraud fell by 700% in 2020 and 2021. “That’s an amazing number,” Davidovich remarked. Such success stemmed from Sardine’s first product: fraud prevention.

Fraud prevention

Sardine sniffed out Kriptomat’s scammers thanks to its powerful user device and behavioral data platform. Rather than focusing on identity information (though Sardine handles that, too), the product zeroes in on suspicious activity beyond those dimensions. Here are a few classic clues:

Name games. No user acting under their authority needs to copy-paste their own name into a sign-up flow. Either your browser pre-fills it based on past behavior, or you type it yourself. However, an “investment advisor” might do precisely this kind of thing.

Expert behavior. A user takes time to understand a new platform. They might click through different tabs, getting lost a few times before they complete an action. A scammer doesn’t operate like this. They’ve likely used an exchange like Kriptomat many times before, meaning they click and scroll with certainty and speed.

Time travelers. Users typically interact with a service from the same time zone as their address. A fraudster might be located in a different country, though. When they access an account, there may be discrepancy between the expected and actual time zone.

Multiple accounts. If you’re a user signing up to Kriptomat for the first time, there’s little chance you would have multiple existing accounts linked to your device. However, this is common for a scammer.

By itself, each action might not be enough to uncover a fraudster. But taken together – and combined with hundreds of other data points – Sardine reliably finds the criminals at work. “It’s not just the information – it’s the how,” said Sardine’s Head of Fraud, Greg Wilson. “It’s how something is typed; how a button is clicked. These actions are the chinks in a fraudster’s armor.”

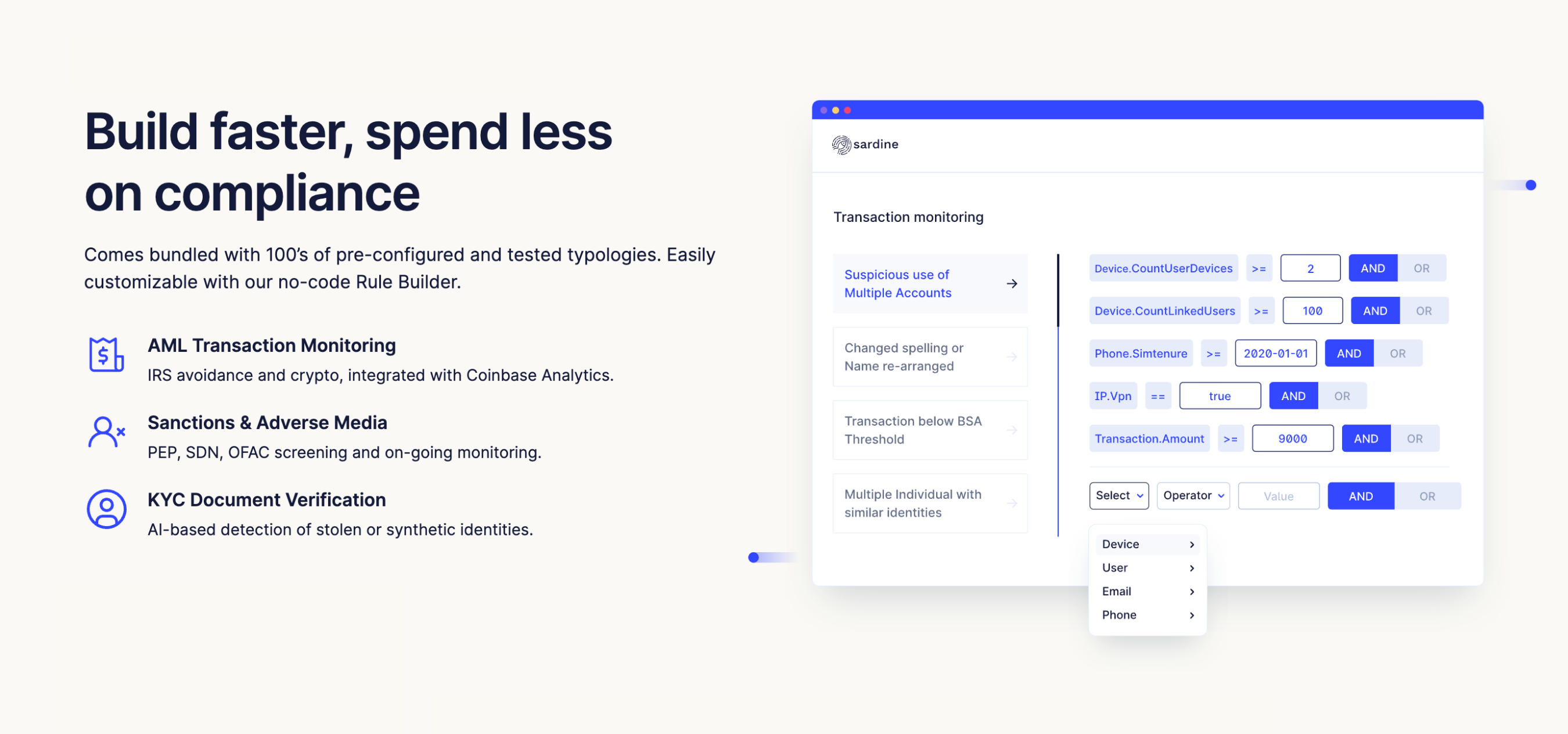

Though this is a highly refined process, Sardine has packaged it simply. An API introduces the company’s technology, and an intuitive platform presents relevant fraud information to monitor. Via a no-code dashboard, customers like Kriptomat can track risk on a user-by-user basis, as well as parsing across dimensions.

Sardine offers hundreds of pre-set rules based on its data and experience, but companies can also edit them to fit their needs. For example, Kriptomat could choose to emphasize time zone discrepancies if it believed this was a strong indication of fraud.

Critically, Sardine’s tool also makes it easy to act. A suspicious user can be disabled in a matter of clicks, sending funds back to the originating bank. This allows a company to move quickly to counteract bad behavior and protect users’ money.

For Kriptomat, Sardine’s product proved revolutionary, but Davidovich’s exchange is far from the only beneficiary. In a little over two years of operation, Sardine has attracted customers like FTX, Brex, Chipper Cash, Relay, and MoonPay. In many cases, Sardine has had an outsized impact. MoonPay, for example, reported that Ranjan’s company had helped reduce fraud by 3x while also reducing friction. AtoB, a freight-focused neobank, reported that of the thousands of data points they look at to combat fraud, Sardine’s were routinely in the top twenty most valuable.

By solving these problems, Sardine gives a company the ability to focus on execution and growth. As co-founder Aditya Goel said: “Companies should be focused on their USP – not drowning in fraud and compliance.”

Payments

Sardine is recognized as a leading fraud prevention service today. In a few years, though, it may be best known as a payments business. Just as Ranjan, Goel, and Shaikh intended, the company has used its fraud prowess to elbow into this competitive market.

Given its founders’ experience, Sardine’s decision to focus on neobanks and crypto companies is unsurprising. The team knows how much friction customers face in using these products. Many readers will have experienced these pains first-hand, finding themselves unable to transfer money to a neobank account or waiting days to purchase crypto on an exchange. Conversion rates in these categories are famously low, with up to 50% of customers stymied. “It’s a coin toss as to whether a transaction goes through,” Goel said of these activities.

As alluded to earlier, this happens primarily because of inadequate risk scoring. Without a precise way of telling a good user from a bad one, financial providers introduce friction, either through waiting times or outright denials.

Perhaps uniquely, Sardine is positioned to solve this problem. Its fraud engine allows the company to better respond to risk. Since it has a sharper sense of who is a danger and who isn’t, it radically improves conversion rates.

Autograph, an NFT platform, partnered with Sardine for this reason. To stop buyers from being turned away, the startup founded by Tom Brady decided to leverage Sardine’s payment infrastructure. It had a profound effect, with Autograph averaging between 94% - 98% conversion rates. “We were able to approve a lot more users,” Goel remarked.

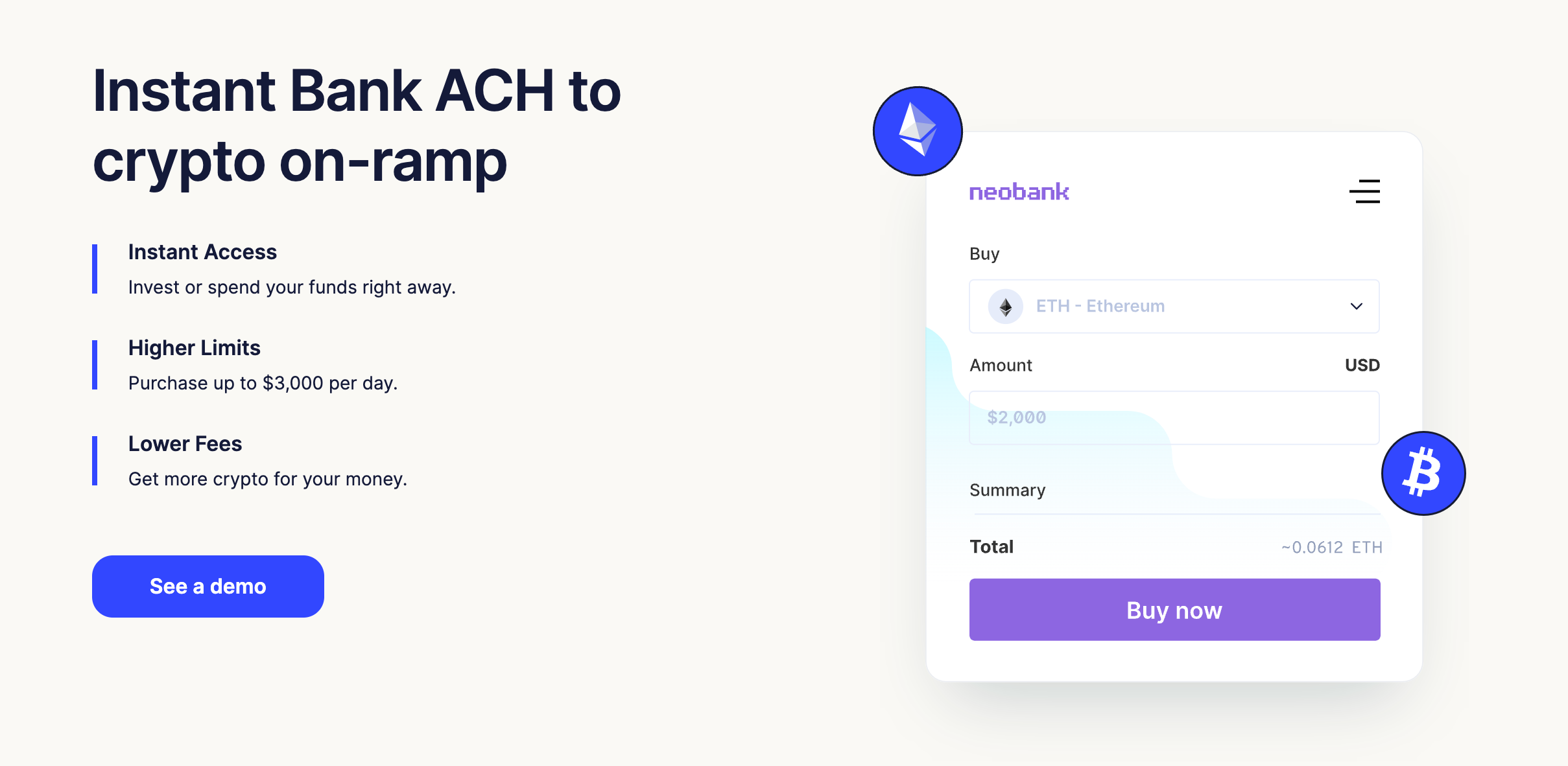

Sardine’s partnership with MetaMask is another example of how it removes friction for crypto companies. With Sardine’s assistance, MetaMask now permits customers to instantly fund their wallets via ACH and then buy crypto. Users don’t need to wait for funds to settle, making for a radically better onboarding and investing experience.

Several other customers have benefited from the reductions in fraud and friction Sardine offers. Ranjan noted that crypto on-ramps like MoonPay, Wyre, and Transak had traditionally avoided instant ACH because “you could easily lose your shirt.” But Sardine has found it can bring ACH conversion up to 95%.

Sardine is so confident in its ability to judge risk better during the payments process that it offers indemnification. Essentially, Sardine takes responsibility for any chargebacks and returns the customer incurs while using its product. “There’s no stronger statement than that,” one industry source said, “That’s putting money where your mouth is.”

As with its fraud prevention suite, Sardine’s product has significant impact. Companies can approve more users, improve the customer experience, and increase revenue. Remarkably, they’re able to do so while incurring no added risk.

Risk insights

Sardine has only just released its risk insights product. But there’s reason to think it could be a powerful addition to an emerging flywheel.

What Ranjan’s team is building is bigger than a product – closer to a “public good,” as Sardine investor Maaria Bajwa described it. The goal is to create something like a modern data consortium. By leveraging Sardine’s risk insights API, customers will access a database of fraud information contributed by other companies. When you query a name or phone number, you’ll see whether that information has been used for fraud anywhere else. In turn, as a corporate customer, you’ll contribute data of your own, which others can rely upon. Ravi Loganathan, Head of Banking Insights, outlined the product’s power in an announcement post:

Insights aims to remove the visibility gap between financial institutions, fintechs, and crypto companies with timely insights to strengthen risk management and remove friction to a wide array of financial products and services.

Soups Ranjan expects the product to be especially valuable on the ACH front. The CEO explained that ACH was designed for payroll usage and was never meant to be deployed to fund accounts. Its proliferation has created new risks that are well-served through coordination.

Per Ranjan, conversations with stakeholders have been positive, with broad interest in a solution like this one. One source, who works at a large crypto exchange, said they see a “benefit in mutually sharing data within the industry.”

Succeeding with the risk insights product could see Sardine accelerate its flywheel. Offering exceptional fraud prevention has made Sardine a better payments provider; expanding its payment network should increase the number of players with which it interacts; the more companies it touches, the better placed it is to extend its risk insights API; and the more data it gathers through risk insights, the better it becomes at fraud prevention.

“It’s the natural next step,” Angela Strange said. “Sardine can say, ‘Do you have fraud problems? Well, our fraud prevention works best if you share your data.’”

Culture: Onions and ownership

Many successful companies pride themselves on their culture. However, when researching Sardine, this strength was mentioned frequently. Ranjan and his co-founders have assembled a stacked team with a desire to build something meaningful.

Leadership

Soups Ranjan is an intriguing CEO. His preference for elevating those that work with him means he maintains a low profile. “He’s got a very humble, likable way about him,” Simon Taylor remarks. “You will immediately underestimate him, as a result.”

Though not the type to give rousing motivational speeches or pontificate in grand terms, Taylor noted that Ranjan has a talent for “pressing for progress, pressing for change,” albeit with trademark subtlety. Often, Ranjan gets into the weeds of a problem to help untangle it, relying on his domain expertise and formidable intelligence. One source described him as in the top 0.1% intellectually.

Aditya Goel is the company’s operational engine. Ranjan described Goel as “extremely detail-oriented,” with a desire to move as quickly as possible. “We have one-week sprints, not two-week sprints. That’s because of Adi.” It doesn’t hurt that Goel is a “payment nerd, through and through,” per Ranjan.

Finally, we come to Zahid Shaikh. Two sources independently described Sardine's Head of Product as “like an onion” in his depth. “The guy is a weapon,” Andrew Steele said. “He’s super quiet but unbelievably technical. You can ask him about any topic, and he will blow your mind.” Ranjan concurred: “The depth of his knowledge is just amazing.”

Masterful recruitment

While Ranjan has obvious strengths, his most outstanding talent is recruitment. Several sources emphasized this ability and the unusual power it gave a company of Sardine’s maturity. “He knows he needs to surround himself with amazing people and give them the rope to do what they need to,” Steele remarked.

Looking at Sardine’s roster, it’s easy to see what Steele's talking about. Many of the company’s employees have deep domain expertise and have either been founders or served in leadership positions. Ravi Loganathan, Head of Banking Insights, previously acted as the Chief Analytics Officer of Early Warning Systems, owner of Zelle. Head of Commercial Development Alex Kushnir started Legend Finance, a crypto savings platform. Simon Taylor co-founded 11:FS, a consultancy focused on fintech. Krisan Nichani, Head of Compliance, served in the same role at neobank Step and crypto project Civic.

“They’re one of the best teams I’ve ever met when it comes to combining fraud, identity, and payments in one package,” Andrew Steele said. The Activant GP recalled sitting down to dinner with the extended Sardine team during the fundraising process and realizing how much talent the startup had amassed. “There were ten people at the table and if any one of them started a business, I would back them,” Steele noted.

Outside of the team’s bonafides, Sardine has fostered a culture of customer obsession and ownership. “The most important thing is that customers come first,” Ranjan said. Beyond that, everyone on the team is encouraged to take responsibility and move the ball forward. “We are mostly doers rather than talkers,” Sardine’s CEO added. Sound Ventures’ Maaria Bajwa echoed that point. “They have a great, great culture. There’s no hierarchy at the senior level – it’s very open and transparent.”

Future: Capitalizing on potential

Sardines do not usually swim very far, but this one has traveled a long way in two and a half years. The fintech has firm product-market fit on its first two offerings, with an ambitious new addition. With little further innovation, Sardine could likely grow its customer and revenue base in time.

Of course, Ranjan will not be satisfied with such an outcome. His team is ready to compete with tech’s biggest businesses in pursuit of scale. Ranjan must nail positioning and cultivate network effects to fulfill Sardine's potential.

Positioning

Payments is not a winner-takes-all business. Large companies might rely on dozens of providers to maximize coverage worldwide. Different industries and modalities favor different players. But any startup that wants to play in online payments does so – at least superficially – under the shadow of Stripe. Like few other companies, the Collisons’ business has shown the ambition and ability to devour fintech use cases across payments, tax, identity, fraud, card issuing, and treasury. That makes them a dangerous adversary for any upstart.

However, there’s reason to believe that Sardine’s offering is sufficiently differentiated and potentially even complementary. For one thing, Sardine’s fraud prevention services are genuinely novel. Customers use the service because they cannot find a suitable alternative elsewhere – including via Stripe. Moreover, Stripe has not traditionally excelled at fraud, with one source suggesting its Radar product was unremarkable. Aditya Goel noted this was not uncommon for the industry: “Fraud has been an afterthought for payments companies. Even for someone like Stripe.”

Because of Sardine’s unique value, Angela Strange suggested the companies might end up working together. “Stripe would be a customer of Sardine,” she said. “Stripe has integrations around the world – if you wanted to nail payment acceptance anywhere, you could use Sardine.”

Even on the payments side of the equation, Sardine and Stripe are not directly analogous. Andrew Steele noted that Stripe had grown by “packaging the card networks,” whereas Sardine focused on ACH and non-card payments. This different focus could allow Ranjan & Co. to capture other use cases. “I’ve seen enough of this space to have a firm belief that it takes a different type of skill to build for ACH and non-card payments,” Steele said.

While Sardine has focused on crypto so far, it should be positioned to capture other significant transactions. Steele explained that for B2B payments, “there needs to be an alternative to cards.” Sardine could become that alternative. Angela Strange also sees potential beyond web3. “Sardine’s early positioning was almost too crypto,” she said, “but the bigger customer set is not crypto.”

Ultimately, if Sardine wants to keep growing, it will need to move aggressively and lean into its points of differentiation. That includes winning ACH and non-card transaction volume and ensuring it is positioned to capture the trillions of dollars that may be spent beyond crypto through standard B2B transactions.

Network effects

To become a generationally important company, Sardine must cultivate network effects. In particular, it must ensure it captures the opportunity it has identified to become the public utility around modern fraud information.

Doing so is no easy task. While the startup has technical and product chops, softer skills will be required to lure institutions, exchanges, and neobanks onto the platform. Financial organizations may be reticent to share their data, even if anonymized. To act as the orchestrator of this network, Sardine will also need to maintain credible neutrality. It cannot be seen favoring one company over another – or itself over other contributors. As Sardine grows and extends its offering, this may take restraint and finesse.

Ultimately, however, such a solution stands to benefit all parties. By fulfilling this role, Sardine can help all of its partners reduce risk and increase revenue. Doing so will empower better consumer experiences across the financial world. This is the kind of multi-stakeholder win that is rarely achievable – and could prove very valuable.

Financial fraud can feel like a game of cat-and-mouse, move and countermove. The scammer devises a cunning ploy; the programmer constructs a clever defense. The scammer finds a hole in the defense; the programmer patches it. This is the dance, and as long as money is made, it will not stop.

The capering quality of this back-and-forth disguises the cost of what is happening. Money is lost; businesses are battered; lives are ruined. Though online money movement can feel like a distant abstraction, there is real human pain in losing it – in having it stolen from you.

Sardine exists to stop such crimes from occurring. It is fintech’s great detective, possessing uncanny observational skills and a rare acuity for reading risk. It is also something greater than that – not just a detective, but a defender. It helps companies deal with bad actors, certainly, but it goes beyond that, stopping fraud from occurring in the first place. Though startups are prone to hyperbole, Sardine can earnestly claim to have changed thousands of lives for the better.

The Generalist’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice. You should always do your own research and consult advisors on these subjects. Our work may feature entities in which Generalist Capital, LLC or the author has invested.